kurtosis

- property AssetList.kurtosis

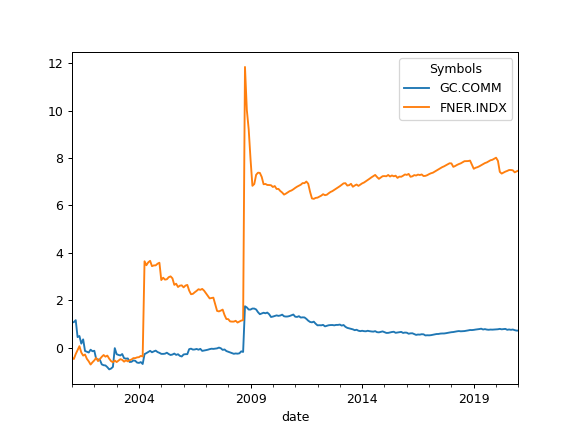

Calculate expanding Fisher (normalized) kurtosis of the return time series for each asset.

Kurtosis is the fourth central moment divided by the square of the variance. It is a measure of the “tailedness” of the probability distribution of a real-valued random variable.

Kurtosis should be close to zero for normal distribution.

- Returns:

- DataFrame

Expanding kurtosis time series for each asset.

See also

skewnessCompute skewness.

skewness_rollingCompute rolling skewness.

kurtosis_rollingCalculate rolling Fisher (normalized) kurtosis.

jarque_beraPerform Jarque-Bera test for normality.

kstestPerform Kolmogorov-Smirnov test for different types of distributions.

Examples

>>> import matplotlib.pyplot as plt

>>> al = ok.AssetList(["GC.COMM", "FNER.INDX"], first_date="2000-01", last_date="2021-01") >>> al.names {'GC.COMM': 'Gold', 'FNER.INDX': 'FTSE NAREIT All Equity REITs'} >>> al.kurtosis.plot() >>> plt.show()