Portfolio

- class Portfolio(assets=None, *, first_date=None, last_date=None, ccy='USD', inflation=True, weights=None, rebalancing_strategy=period month abs_deviation NaN rel_deviation NaN dtype: str, symbol=None)

Bases:

ListMakerInvestment portfolio.

An investment portfolio is a type of financial asset (same as stocks, ETFs, mutual funds, currencies, etc.). The arguments are similar to AssetList, but Portfolio additionally has:

weights

rebalancing_strategy

symbol

Portfolio is defined by the investment strategy, which includes:

asset allocation (financial assets and their proportions in the portfolio)

the rebalancing strategy (rebalancing_strategy parameter)

Rebalancing is the action of bringing the portfolio that has deviated away from the original target asset allocation back into line. After rebalancing, the portfolio assets have the original weights.

- Parameters:

- assetslist, default None

List of assets. Could include tickers or asset-like objects (Asset, Portfolio). If None, a single-asset list with a default ticker is used.

- first_datestr, default None

First date of monthly return time series. If None, the first date is calculated automatically as the oldest available date for the listed assets.

- last_datestr, default None

Last date of monthly return time series. If None, the last date is calculated automatically as the newest available date for the listed assets.

- ccystr, default ‘USD’

Base currency for the list of assets. All risk metrics and returns are adjusted to the base currency.

- inflationbool, default True

Defines whether to take inflation data into account in the calculations. Including inflation could limit available data (first_date, last_date) as the inflation data is usually published with a one-month delay. With inflation=False, some properties like real return are not available.

- weightslist of float, default None

List of asset weights. The weight of an asset is the percent of an investment portfolio that corresponds to the asset. If None, an equally weighted portfolio is created (all weights are equal).

- rebalancing_strategyRebalance, default Rebalance(period=”month”)

Rebalancing strategy for an investment portfolio. The strategy is defined by:

period (rebalancing frequency): predetermined time intervals when the investor rebalances the portfolio. If “none”, asset weights are not rebalanced.

abs_deviation: the absolute deviation allowed for the asset weights in the portfolio.

rel_deviation: the relative deviation allowed for the asset weights in the portfolio.

- symbolstr, default None

Text symbol of portfolio. It is similar to tickers but have a namespace information. Portfolio symbol must end with .PF (all_weather_portfolio.PF). If None, a random symbol is generated (portfolio_7802.PF).

Methods & Attributes

annual_return_ts([return_type])Calculate annual rate of return time series for portfolio.

Show assets monthly close time series adjusted to the base currency.

Calculate last twelve months (LTM) dividend yield time series (monthly) for each asset.

Rate of return monthly time series for all assets.

Portfolio size monthly time series.

Return the base currency.

describe([years])Generate descriptive statistics for the portfolio.

Calculate Diversification Ratio for the portfolio.

Calculate last twelve months (LTM) dividend yield time series for the portfolio.

Calculate last twelve months (LTM) dividend yield annual time series.

Calculate portfolio dividends monthly time series.

Return calendar year dividends sum time series for each asset.

Calculate drawdowns time series for the portfolio.

get_cagr([period, real])Calculate the expanding portfolio Compound Annual Growth Rate (CAGR) time series.

get_cumulative_return([period, real])Calculate the expanding cumulative return time series for the portfolio.

get_cvar_historic([time_frame, level])Calculate historic Conditional Value at Risk (CVAR, expected shortfall) for the portfolio.

Calculate monthly geometric mean return for the portfolio.

get_rolling_cagr([window, real])Calculate rolling CAGR (Compound Annual Growth Rate) for the portfolio.

get_rolling_cumulative_return([window, real])Calculate rolling cumulative return.

get_sharpe_ratio([rf_return])Calculate Sharpe ratio.

get_sortino_ratio([t_return])Calculate Sortino ratio for the portfolio with specified target return.

get_var_historic([time_frame, level])Calculate historic Value at Risk (VaR) for the portfolio.

Calculate annualized mean return (arithmetic mean) for the portfolio rate of return time series.

Calculate monthly mean return (arithmetic mean) for the portfolio rate of return time series.

Return text name of portfolio.

Calculate the number of securities monthly time series for the portfolio assets.

URL link to portfolio at okama.io.

percentile_cagr(years[, percentiles])Calculate given percentiles for portfolio rolling CAGR distribution from the historical data.

percentile_inverse_cagr([years, score])Compute the percentile rank of a score (CAGR value).

plot_assets([kind, tickers, pct_values, xy_text])Plot asset points on the risk-return chart with annotations.

Calculate price drawdowns time series for the portfolio.

Calculate real (inflation-adjusted) drawdowns time series for the portfolio.

Calculate annualized real mean return (arithmetic mean) for the rate of return time series.

Time series with the dates of rebalancing events.

Return rebalancing strategy of the portfolio.

Get recovery period time series for the portfolio value.

Calculate annualized risk expanding time series for portfolio.

Calculate monthly risk expanding time series for Portfolio.

Calculate monthly rate of return time series for portfolio considering rebalancing strategy.

Return semideviation annualized value for portfolio rate of return time series.

Calculate semi-deviation monthly value for portfolio rate of return time series.

Return a text symbol of portfolio.

Return a list of used financial symbols.

Return table with security name, ticker, weight for assets in the portfolio.

Return a list of used tickers (symbols without a namespace).

tracking_error(benchmark[, rolling_window, ...])Calculate ex-post tracking error time series of the portfolio against a benchmark.

Calculate wealth index time series for the portfolio and accumulated inflation.

Calculate wealth index time series for the portfolio, all assets and accumulated inflation.

Assets weights in portfolio.

Calculate assets weights time series considering rebalancing strategy.

- property weights

Assets weights in portfolio.

If not defined equal weights are used for each asset.

Weights must be a list (or tuple) of float values.

- Returns:

- list or tuple

Values for the weights of assets in portfolio.

Examples

>>> x = ok.Portfolio(["SPY.US", "BND.US"]) >>> x.weights [0.5, 0.5]

- property weights_ts

Calculate assets weights time series considering rebalancing strategy.

The weights of assets in Portfolio are not constant if rebalancing_period is different from ‘month’.

- Returns:

- DataFrame

Weights of assets time series.

Examples

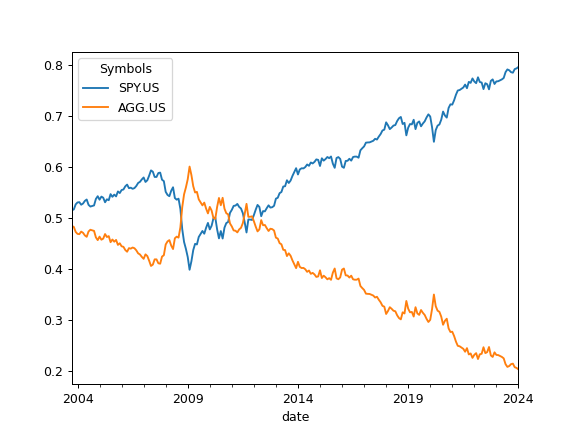

>>> import matplotlib.pyplot as plt

>>> reb_period = ok.Rebalance(period="none") # The Portfolio is not rebalanced. >>> pf = ok.Portfolio(["SPY.US", "AGG.US"], weights=[0.5, 0.5], rebalancing_strategy=reb_period) >>> pf.weights_ts.plot() >>> plt.show()

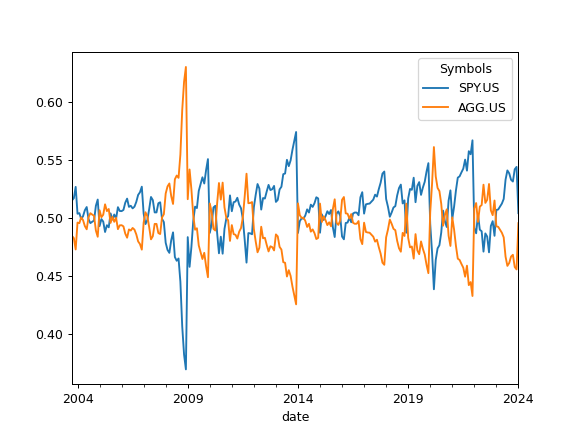

The weights of assets time series will differ significantly if the portfolio rebalancing_period is 1 year.

>>> pf.rebalancing_strategy = ok.Rebalance(period="year") # set a new rebalancing period >>> pf.weights_ts.plot() >>> plt.show()

- property rebalancing_events

Time series with the dates of rebalancing events.

Each event has the type of rebalancing event: - calendar (calendar event) - abs (rebalancing by absolute deviation) - rel (rebalancing by relative deviation)

- Returns:

- DataFrame

Dates of rebalancing events time series.

Examples

>>> pf = ok.Portfolio( ... assets=["SPY.US", "AGG.US"], ... weights=[0.5, 0.5], ... rebalancing_strategy=ok.Rebalance(period="year", abs_deviation=0.05), ... ) >>> pf.rebalancing_events date 2004-05 calendar 2005-05 calendar 2006-05 calendar 2007-05 calendar 2008-05 calendar ... 2020-05 calendar 2020-11 abs 2021-05 calendar 2022-05 calendar 2023-05 calendar Name: event, Length: 21, dtype: object

- property rebalancing_strategy

Return rebalancing strategy of the portfolio.

Rebalancing is the process by which an investor restores their portfolio to its target allocation by selling and buying assets. After rebalancing all the assets have original weights.

Rebalancing period (rebalancing frequency) is predetermined time intervals when the investor rebalances the portfolio.

- Returns:

- Rebalance

Portfolio rebalancing strategy.

Examples

>>> pf = ok.Portfolio( ... assets=["SPY.US", "AGG.US"], ... weights=[0.5, 0.5], ... rebalancing_strategy=ok.Rebalance(period="year", abs_deviation=0.05), ... ) >>> pf.rebalancing_strategy Rebalance(period='year', abs_deviation=0.05, rel_deviation=None)

- property symbol

Return a text symbol of portfolio.

Symbols are similar to tickers but have a namespace information:

SPY.US is a symbol

SPY is a ticker

Portfolios have ‘.PF’ as a namespace.

- Returns:

- str

Text symbol of the portfolio.

Examples

>>> p = ok.Portfolio() >>> p.symbol # a randomly generated symbol will be shown 'portfolio_5312.PF'

>>> p.symbol = "spy_portfolo.PF" # The symbol can be customized after initialization

New Portfolio can have a custom symbol.

>>> p = ok.Portfolio(symbol="aggressive.PF") >>> p.symbol 'aggressive.PF'

- property name

Return text name of portfolio.

For Portfolio name is equal to symbol.

- Returns:

- str

Text name of the portfolio.

>>> p = ok.Portfolio() ..

>>> p.name ..

- ‘portfolio_5312.PF’

- property ror

Calculate monthly rate of return time series for portfolio considering rebalancing strategy.

- Returns:

- Series

Rate of return monthly time series for the portfolio.

Examples

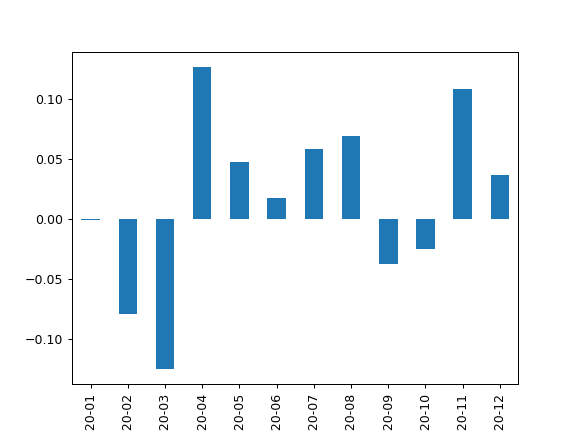

>>> pf = ok.Portfolio(first_date="2020-01", last_date="2020-12") >>> pf.ror Date 2020-01 -0.0004 2020-02 -0.0792 2020-03 -0.1249 2020-04 0.1270 2020-05 0.0476 2020-06 0.0177 2020-07 0.0589 2020-08 0.0698 2020-09 -0.0374 2020-10 -0.0249 2020-11 0.1088 2020-12 0.0370 Freq: M, Name: portfolio_4669.PF, dtype: float64

>>> import matplotlib.pyplot as plt

>>> pf.ror.plot(kind="bar") >>> plt.show()

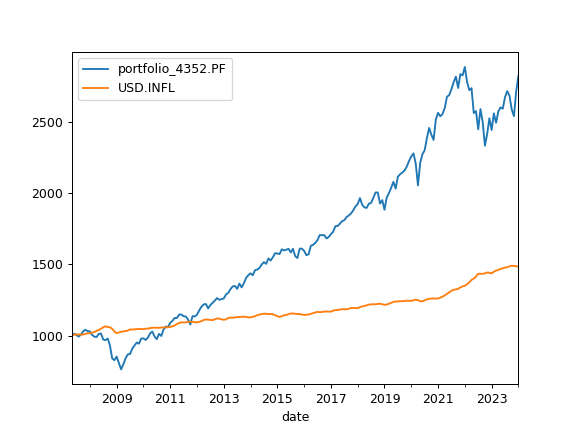

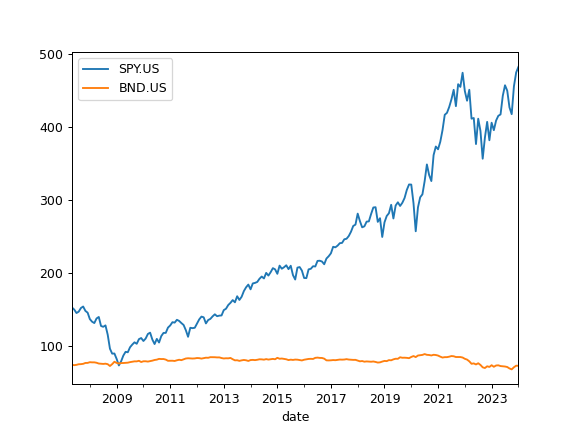

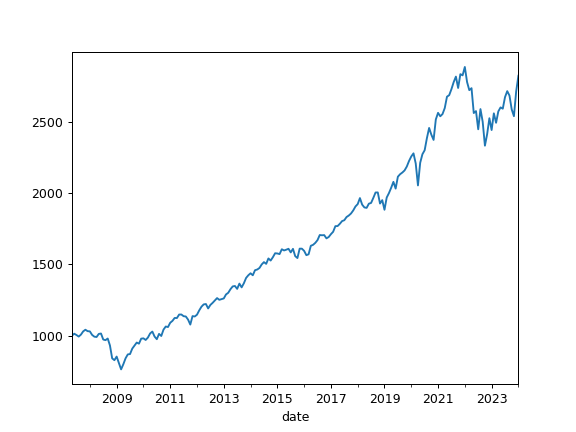

- property wealth_index

Calculate wealth index time series for the portfolio and accumulated inflation.

Wealth index (Cumulative Wealth Index) is a time series that presents the value of portfolio over historical time period. Accumulated inflation time series is added if inflation=True in the Portfolio.

Wealth index is obtained from the accumulated return multiplied by the initial investments. That is: 1000 * (Acc_Return + 1) Initial investments are taken as 1000 units of the Portfolio base currency.

- Returns:

- DataFrame

Time series of wealth index values for portfolio and accumulated inflation.

Examples

>>> import matplotlib.pyplot as plt

>>> x = ok.Portfolio(["SPY.US", "BND.US"]) >>> x.wealth_index.plot() >>> plt.show()

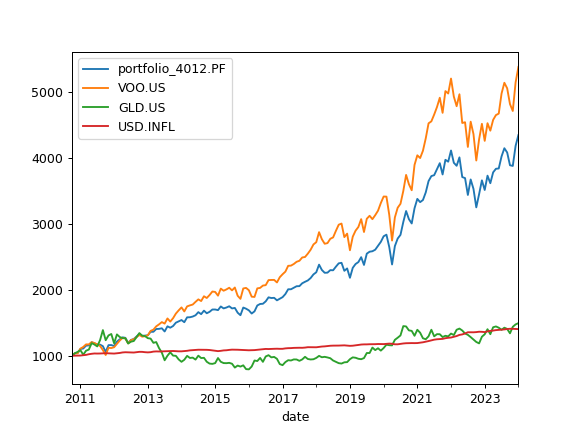

- property wealth_index_with_assets

Calculate wealth index time series for the portfolio, all assets and accumulated inflation.

Cash flows are not taken into account.

Wealth index (Cumulative Wealth Index) is a time series that presents the value of portfolio over historical time period. Accumulated inflation time series is added if inflation=True in the Portfolio.

Wealth index is obtained from the accumulated return multiplied by the initial investments. initial_amount_pv * (Acc_Return + 1)

- Returns:

- DataFrame

Time series of wealth index values for portfolio, each asset and accumulated inflation.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["VOO.US", "GLD.US"], weights=[0.8, 0.2]) >>> pf.wealth_index_with_assets.plot() >>> plt.show()

- property mean_return_monthly

Calculate monthly mean return (arithmetic mean) for the portfolio rate of return time series.

Mean return calculated for the full history period.

- Returns:

- float

Mean return value.

Examples

>>> pf = ok.Portfolio(["ISF.LSE", "XGLE.LSE"], weights=[0.6, 0.4], ccy="GBP") >>> pf.mean_return_monthly 0.0001803312727272665

- property mean_return_annual

Calculate annualized mean return (arithmetic mean) for the portfolio rate of return time series.

Mean return calculated for the full history period.

- Returns:

- float

Mean return value.

Examples

>>> pf = ok.Portfolio(["XCS6.XETR", "PHAU.LSE"], weights=[0.85, 0.15], ccy="USD") >>> pf.names {'XCS6.XETR': 'Xtrackers MSCI China UCITS ETF 1C', 'PHAU.LSE': 'WisdomTree Physical Gold'} >>> pf.mean_return_annual 0.09005826844072184

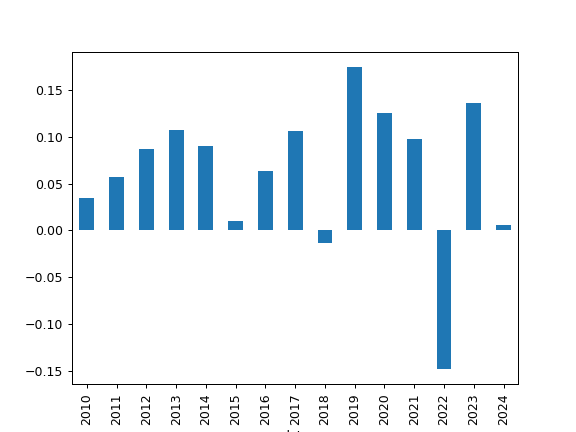

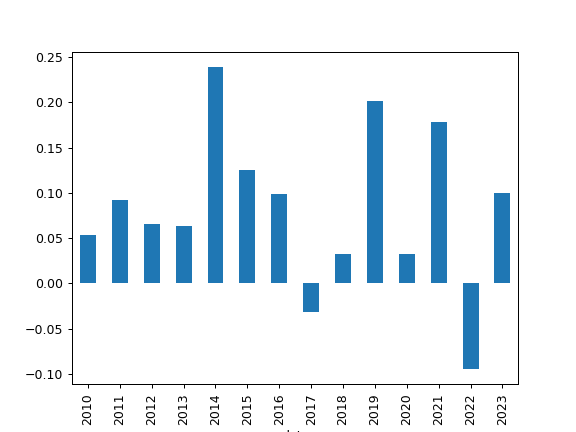

- annual_return_ts(return_type='cagr')

Calculate annual rate of return time series for portfolio.

Rate of return is calculated for each calendar year.

- Parameters:

- return_type{‘cagr’, ‘arithmetic_mean’}, default ‘cagr’

Method used to calculate annual returns.

- Returns:

- Series

Calendar annual rate of return time series.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["VOO.US", "AGG.US"], weights=[0.4, 0.6]) >>> pf.annual_return_ts().plot(kind="bar") >>> plt.show()

Plot annual returns for portfolio with EUR as the base currency.

>>> pf = ok.Portfolio(["VOO.US", "AGG.US"], weights=[0.4, 0.6], ccy="EUR") >>> pf.annual_return_ts().plot(kind="bar") >>> plt.show()

- get_cagr(period=None, real=False)

Calculate the expanding portfolio Compound Annual Growth Rate (CAGR) time series.

The expanding CAGR at each month is the annualized rate of return required for the investment to grow from its initial value to its value at that month, assuming all incomes were reinvested. The last row contains the CAGR over the full selected period.

Inflation adjusted annualized returns (real CAGR) are shown with real=True option. Annualized inflation is calculated for the same period if inflation=True in the Portfolio.

- Parameters:

- periodint, default None

CAGR trailing period in years. If None, use the full available period.

- realbool, default False

CAGR is adjusted for inflation (real CAGR) if True. Portfolio should be initiated with inflation=True for real CAGR.

- Returns:

- DataFrame

Time series of expanding portfolio CAGR and annualized inflation (if inflation=True in Portfolio and real=False).

Notes

CAGR is not defined for periods less than 1 year. The first 11 rows are filled with NaN values.

Examples

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], weights=[0.6, 0.4], ccy="USD", inflation=True) >>> pf.get_cagr(period=5).tail()

The last row contains the CAGR values over the full selected period.

To get inflation adjusted annualized return (real CAGR) add real=True option:

>>> pf.get_cagr(period=5, real=True).tail()

- get_rolling_cagr(window=12, real=False)

Calculate rolling CAGR (Compound Annual Growth Rate) for the portfolio.

- Parameters:

- windowint, default 12

Size of the moving window in months. Window size should be at least 12 months for CAGR.

- realbool, default False

CAGR is adjusted for inflation (real CAGR) if True. Portfolio should be initiated with Inflation=True for real CAGR.

- Returns:

- DataFrame

Time series of rolling CAGR and mean inflation (optionally).

Notes

CAGR is not defined for periods less than 1 year (NaN values are returned).

Examples

>>> x = ok.Portfolio(["SPY.US", "BND.US"], ccy="EUR", inflation=True) >>> x.get_rolling_cagr(window=5 * 12, real=True) portfolio_... date ... ...

- get_monthly_geometric_mean_return()

Calculate monthly geometric mean return for the portfolio.

The geometric mean return is the constant periodic return that would produce the same final value as a sequence of varying periodic returns when compounded over time.

- Returns:

- float

Monthly geometric mean return value.

Examples

>>> pf = ok.Portfolio(["SPY.US", "AGG.US"], weights=[0.6, 0.4]) >>> pf.get_monthly_geometric_mean_return() 0.005321

- get_cumulative_return(period=None, real=False)

Calculate the expanding cumulative return time series for the portfolio.

The cumulative return is the total compounded change in the portfolio price from the start of the selected period up to and including each subsequent month. The last row contains the cumulative return over the full selected period.

Inflation adjusted cumulative returns (real cumulative returns) are shown with real=True option. Inflation data is taken from the same period if inflation=True in the Portfolio.

- Parameters:

- periodstr or int or None, default None

Trailing period in years. None - full time cumulative return. ‘YTD’ - (Year To Date) period of time beginning the first day of the calendar year up to the last month.

- realbool, default False

Cumulative return is adjusted for inflation (real cumulative return) if True. Portfolio should be initiated with Inflation=True for real cumulative return.

- Returns:

- DataFrame

Time series of cumulative return for the portfolio and cumulative inflation (if inflation=True in Portfolio and real=False).

Examples

>>> pf = ok.Portfolio(["BTC-USD.CC", "LTC-USD.CC"], weights=[0.8, 0.2], last_date="2021-03") >>> pf.get_cumulative_return(period=2, real=True).tail() portfolio_6232.PF 2020-11 3.624500 2020-12 5.125700 2021-01 7.328400 2021-02 8.612000 2021-03 9.393810

The last row contains the cumulative return over the full selected period.

- get_rolling_cumulative_return(window=12, real=False)

Calculate rolling cumulative return.

The cumulative return is the total change in the portfolio price.

- Parameters:

- windowint, default 12

Size of the moving window in months.

- realbool, default False

Cumulative return is adjusted for inflation (real cumulative return) if True. Portfolio should be initiated with Inflation=True for real cumulative return.

- Returns:

- DataFrame

Time series of rolling cumulative return and inflation (optional).

Examples

>>> pf = ok.Portfolio( ... ["SPY.US", "AGG.US", "GLD.US"], ... weights=[0.6, 0.35, 0.05], ... rebalancing_strategy=ok.Rebalance(period="year"), ... ) >>> pf.get_rolling_cumulative_return(window=24, real=True) portfolio_9012.PF 2006-11 0.125728 2006-12 0.104348 2007-01 0.129601 2007-02 0.110680 2007-03 0.132610 ... 2021-03 0.263755 2021-04 0.275474 2021-05 0.322736 2021-06 0.264963 2021-07 0.273801 [177 rows x 1 columns]

- property close_monthly

Portfolio size monthly time series.

Portfolio size is shown in base currency units. It is similar to the close value of an asset. Initial portfolio value is equal to 1000 units of base currency.

- Returns:

- pd.Series

Monthly portfolio size time series.

Notes

‘close_mothly’ shows the same output as the ‘wealth_index’. This property is required as Portfolio must have the same attributes as an Asset.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD") >>> pf.close_monthly.plot() >>> plt.show()

- property number_of_securities

Calculate the number of securities monthly time series for the portfolio assets.

The number of securities in the Portfolio is changing over time as the dividends are reinvested. Portfolio rebalancing also affects the number of securities.

Initial number of securities depends on the portfolio size in base currency (1000 units).

- Returns:

- DataFrame

Number of securities monthly time series for the portfolio assets.

Examples

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="07-2021") >>> pf.number_of_securities SPY.US BND.US Date 2007-05 3.261153 6.687174 2007-06 3.337216 6.758447 2007-07 3.407015 6.643519 2007-08 3.410268 6.663862 2007-09 3.372630 6.798730 ... ... 2021-03 3.273521 15.313911 2021-04 3.204779 15.685601 2021-05 3.196768 15.749127 2021-06 3.186124 15.879056 2021-07 3.166335 16.003569 [171 rows x 2 columns]

- property dividends

Calculate portfolio dividends monthly time series.

Portfolio dividends are obtained by summing asset dividends adjusted to the base currency. Dividends size depends on the portfolio value and number of securities.

- Returns:

- Series

Portfolio dividends monthly time series.

Examples

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="07-2021") >>> pf.dividends 2007-05 0.849271 2007-06 3.928855 2007-07 1.551262 2007-08 2.023148 2007-09 4.423416 ... 2021-03 6.155337 2021-04 3.019478 2021-05 2.056836 2021-06 6.519521 2021-07 2.114071 Freq: M, Name: portfolio_2951.PF, Length: 171, dtype: float64

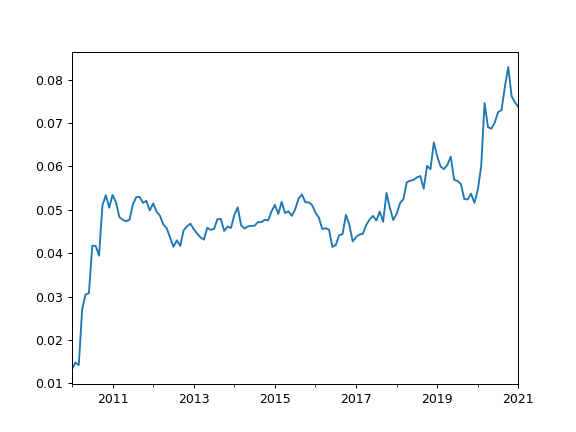

- property dividend_yield

Calculate last twelve months (LTM) dividend yield time series for the portfolio. Time series has monthly values.

Portfolio dividend yield is a weighted sum of the assets dividend yields (adjusted to the portfolio base currency).

For an asset LTM dividend yield is the sum trailing twelve months of common dividends per share divided by the current price per share.

- Returns:

- Series

Portfolio LTM dividend yield monthly time series.

Examples

>>> pf = ok.Portfolio(["T.US", "XOM.US"], weights=[0.8, 0.2], first_date="2010-01", last_date="2021-01", ccy="USD") >>> pf.dividend_yield 2010-01 0.013249 2010-02 0.014835 2010-03 0.014257 ... 2020-11 0.076132 2020-12 0.074743 2021-01 0.073643 Freq: M, Name: portfolio_8836.PF, Length: 133, dtype: float64

>>> import matplotlib.pyplot as plt

>>> pf.dividend_yield.plot() >>> plt.show()

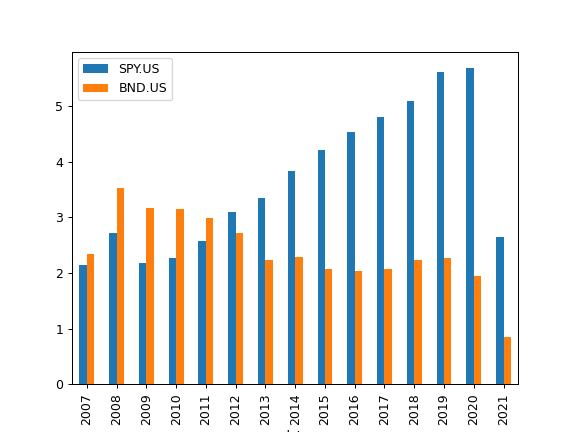

- property dividends_annual

Return calendar year dividends sum time series for each asset.

- Returns:

- DataFrame

Annual dividends time series for each asset.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="07-2021") >>> pf.dividends_annual.plot(kind="bar") >>> plt.show()

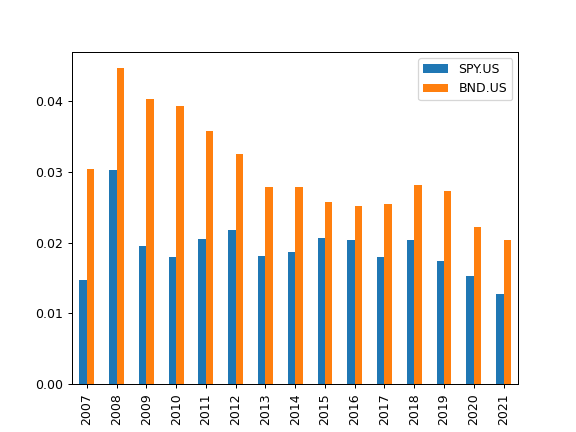

- property dividend_yield_annual

Calculate last twelve months (LTM) dividend yield annual time series.

Time series is based on the dividend yield for the end of calendar year.

LTM dividend yield is the sum trailing twelve months of common dividends per share divided by the current price per share.

All yields are calculated in the asset list base currency after adjusting the dividends and price time series. Forecasted (future) dividends are removed.

- Returns:

- DataFrame

Time series of LTM dividend yield for each asset.

See also

dividend_yieldDividend yield time series.

dividends_annualCalendar year dividends time series.

dividend_paying_yearsNumber of years of consecutive dividend payments.

dividend_growing_yearsNumber of years when the annual dividend was growing.

get_dividend_mean_yieldArithmetic mean for annual dividend yield.

get_dividend_mean_growth_rateGeometric mean of annual dividends growth rate.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="07-2021") >>> pf.dividend_yield_annual.plot(kind="bar") >>> plt.show()

- property assets_dividend_yield

Calculate last twelve months (LTM) dividend yield time series (monthly) for each asset.

LTM dividend yield is the sum trailing twelve months of common dividends per share divided by the current price per share.

All yields are calculated in the asset list base currency after adjusting the dividends and price time series. Forecasted (future) dividends are removed. Zero value time series are created for assets without dividends.

- Returns:

- DataFrame

Monthly time series of LTM dividend yield for each asset.

See also

dividend_yield_annualCalendar year dividend yield time series.

dividends_annualCalendar year dividends time series.

dividend_paying_yearsNumber of years of consecutive dividend payments.

dividend_growing_yearsNumber of years when the annual dividend was growing.

get_dividend_mean_yieldArithmetic mean for annual dividend yield.

get_dividend_mean_growth_rateGeometric mean of annual dividends growth rate.

Examples

>>> x = ok.AssetList(["T.US", "XOM.US"], first_date="1984-01", last_date="1994-12") >>> x.dividend_yield T.US XOM.US 1984-01 0.000000 0.000000 1984-02 0.000000 0.002597 1984-03 0.002038 0.002589 1984-04 0.001961 0.002346 ... ... 1994-09 0.018165 0.012522 1994-10 0.018651 0.011451 1994-11 0.018876 0.012050 1994-12 0.019344 0.011975 [132 rows x 2 columns]

- property real_mean_return

Calculate annualized real mean return (arithmetic mean) for the rate of return time series.

Real rate of return is adjusted for inflation. Real return is defined if there is an inflation=True option in Portfolio.

- Returns:

- float

Annualized value of the mean for the real rate of return time series.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"]) >>> pf.real_mean_return 0.3088967455111862

- property risk_monthly

Calculate monthly risk expanding time series for Portfolio.

Monthly risk of portfolio is a standard deviation of the rate of return time series. Standard deviation (sigma) is normalized by N-1.

- Returns:

- Series

Standard deviation of the monthly return expanding time series.

See also

risk_annualCalculate annualized risks.

semideviation_monthlyCalculate semideviation monthly values.

semideviation_annualCalculate semideviation annualized values.

get_var_historicCalculate historic Value at Risk (VaR).

get_cvar_historicCalculate historic Conditional Value at Risk (CVaR).

drawdownsCalculate drawdowns.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"]) >>> pf.risk_monthly date 1986-05 0.020117 1986-06 0.122032 1986-07 0.130113 1986-08 0.116642 ... 2023-08 0.092875 2023-09 0.092861 2023-10 0.092759 2023-11 0.092763 2023-12 0.092665 Freq: M, Name: portfolio_1094.PF, Length: 453, dtype: float64

- property risk_annual

Calculate annualized risk expanding time series for portfolio.

Risk is a standard deviation of the rate of return.

Annualized risk is calculated for rate of retirun time series for the sample from ‘first_date’ to ‘last_date’.

- Returns:

- Series

Annualized standard deviation of the monthly return expanding time series.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"]) >>> pf.risk_annual date 1986-05 0.285175 1986-06 0.890909 1986-07 0.616876 1986-08 0.632270 1986-09 0.509642 ... 2023-08 0.428297 2023-09 0.427350 2023-10 0.426961 2023-11 0.427930

- property semideviation_monthly

Calculate semi-deviation monthly value for portfolio rate of return time series.

Semi-deviation (Downside risk) is the risk of the return being below the expected return.

- Returns:

- float

Semi-deviation monthly value for portfolio rate of return time series.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"], last_date="2024-12") >>> pf.semideviation_monthly 0.057319735856567695

- property semideviation_annual

Return semideviation annualized value for portfolio rate of return time series.

Semi-deviation (Downside risk) is the risk of the return being below the expected return.

- Returns:

- float

Annualized semi-deviation monthly value for portfolio rate of return time series.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"], last_date="2024-12") >>> pf.semideviation_annual 0.1985613895600056

- get_var_historic(time_frame=12, level=1)

Calculate historic Value at Risk (VaR) for the portfolio.

The VaR calculates the potential loss of an investment with a given time frame and confidence level. Loss is a positive number (expressed in cumulative return). If VaR is negative there are expected gains at this confidence level.

- Parameters:

- time_frameint, default 12

Time frame for VAR. Default is 12 months.

- levelint, default 1

Confidence level in percents. Default value is 1%.

- Returns:

- float

Historic Value at Risk (VaR) value for the portfolio.

Examples

>>> x = ok.Portfolio(["SP500TR.INDX", "SP500BDT.INDX"], last_date="2021-01") >>> x.get_var_historic(time_frame=12, level=1) 0.24030006476701732

- get_cvar_historic(time_frame=12, level=1)

Calculate historic Conditional Value at Risk (CVAR, expected shortfall) for the portfolio.

CVaR is the average loss over a specified time period of unlikely scenarios beyond the confidence level. Loss is a positive number (expressed in cumulative return). If CVaR is negative there are expected gains at this confidence level.

- Parameters:

- time_frameint, default 12

Time period size in months.

- levelint, default 1

Confidence level in percents to calculate the VaR. Default value is 1% (1% quantile).

- Returns:

- float

Historic Conditional Value at Risk (CVAR, expected shortfall) value for the portfolio.

Examples

>>> x = ok.Portfolio(["USDEUR.FX", "BTC-USD.CC"], last_date="2021-01") >>> x.get_cvar_historic(time_frame=2, level=1) 0.3566909250442616

- property drawdowns

Calculate drawdowns time series for the portfolio.

The drawdown is the percent decline from a previous peak in wealth index.

- Returns:

- Series

Drawdowns time series for the portfolio

- property real_drawdowns

Calculate real (inflation-adjusted) drawdowns time series for the portfolio.

The real drawdown is the percent decline from a previous peak in the inflation-adjusted wealth index. Portfolio should be initiated with inflation=True for real drawdowns.

- Returns:

- Series

Real drawdowns time series for the portfolio.

See also

drawdownsCalculate drawdowns (not adjusted for inflation).

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], inflation=True, last_date="2021-08") >>> pf.real_drawdowns.plot() >>> plt.show()

- property price_drawdowns

Calculate price drawdowns time series for the portfolio.

The price drawdown is the percent decline from a previous peak in the portfolio price index. The price index is built from the assets close prices (not adjusted for dividends) with the same weights and rebalancing strategy as the portfolio, hence price drawdowns may significantly differ from drawdowns (based on total return) for portfolios with high dividend assets.

The price index is anchored at the first month of the period, so price drawdowns cover the same months as drawdowns.

- Returns:

- Series

Price drawdowns time series for the portfolio.

See also

drawdownsCalculate drawdowns from total return (with dividends reinvested).

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="2021-08") >>> pf.price_drawdowns.plot() >>> plt.show()

- property recovery_period

Get recovery period time series for the portfolio value.

The recovery period (drawdown duration) is the number of months to reach the value of the last maximum.

- Returns:

- pd.Series

Recovery period time series for the portfolio value

See also

drawdownsCalculate drawdowns time series.

Notes

The largest recovery period does not necessary correspond to the max drawdown.

Examples

>>> pf = ok.Portfolio(["SPY.US", "AGG.US"], weights=[0.5, 0.5]) >>> pf.recovery_period.nlargest() date 2010-10 35 2004-10 7 2012-01 7 2019-03 6 2018-07 5 Freq: M, Name: portfolio_5724.PF, dtype: int32

- describe(years=(1, 5, 10))

Generate descriptive statistics for the portfolio.

Statistics includes:

YTD (Year To date) compound return

CAGR for a given list of periods and full available period

Annualized mean rate of return (full available period)

LTM Dividend yield - last twelve months dividend yield

Risk metrics (full available period):

risk (standard deviation)

CVAR (timeframe is 1 year)

max drawdowns (and dates)

- Parameters:

- yearstuple of int, default (1, 5, 10)

List of periods for CAGR statistics.

- Returns:

- DataFrame

Table of descriptive statistics for the portfolio.

See also

get_cumulative_returnCalculate cumulative return.

get_cagrCalculate portfolio Compound Annual Growth Rate (CAGR).

dividend_yieldCalculate dividend yield (LTM).

risk_annualReturn annualized risks (standard deviation).

get_cvar_historicCalculate historic Conditional Value at Risk (CVAR, expected shortfall).

drawdownsCalculate drawdowns.

Examples

>>> pf = ok.Portfolio(["SPY.US", "BND.US"], ccy="USD", last_date="07-2021") >>> pf.describe(years=[2, 5, 7]) # 'years' customizes the timeframe for the CAGR property period portfolio_2951.PF inflation 0 compound return YTD 0.084098 0.048154 1 CAGR 2 years 0.141465 0.031566 2 CAGR 5 years 0.102494 0.025582 3 CAGR 7 years 0.091694 0.019656 4 CAGR 14 years, 3 months 0.074305 0.019724 5 Dividend yield LTM 0.016504 NaN 6 Risk 14 years, 3 months 0.086103 NaN 7 CVAR 14 years, 3 months 0.214207 NaN 8 Max drawdown 14 years, 3 months -0.266915 NaN 9 Max drawdown date 14 years, 3 months 2009-02 NaN

- property table

Return table with security name, ticker, weight for assets in the portfolio.

When at least one asset has a local name, an additional ‘local name’ column is inserted between ‘asset name’ and ‘ticker’.

- Returns:

- DataFrame

Security name - ticker - weight table.

Examples

>>> pf = ok.Portfolio(["MSFT.US", "AAPL.US"]) >>> pf.table asset name ticker weights 0 Microsoft Corporation MSFT.US 0.5 1 Apple Inc AAPL.US 0.5

>>> pf = ok.Portfolio(["SBER.MOEX", "MSFT.US"]) >>> pf.table asset name local name ticker weights 0 Sberbank Сбербанк SBER.MOEX 0.5 1 Microsoft Corporation Microsoft Corporation MSFT.US 0.5

- percentile_inverse_cagr(years=1, score=0)

Compute the percentile rank of a score (CAGR value).

Percentile rank can be calculated for a historical distribution of CAGR.

If percentile_inverse of, for example, 0% (CAGR value) is equal to 8% for 1 year time frame it means that 8% of the CAGR values in the distribution are negative in 1 year periods. Or in other words the probability of getting negative result after 1 year of investments is 8%.

- Parameters:

- yearsint, default 1

Period length (time frame) in years when CAGR is calculated.

- scorefloat, default 0

Score that is compared to the elements in CAGR array.

- Returns:

- float

Percentile-position of score (0-100) relative to distribution.

Examples

>>> pf = ok.Portfolio( ... ["SPY.US", "AGG.US", "GLD.US"], ... weights=[0.60, 0.35, 0.05], ... rebalancing_strategy=ok.Rebalance(period="year"), ... ) >>> pf.percentile_inverse_cagr(score=0, years=1) 18.08 The probability of getting negative result (score=0) in 1 year period for historical distribution.

- property assets_close_monthly

Show assets monthly close time series adjusted to the base currency.

- Returns:

- DataFrame

Assets monthly close time series adjusted to the base currency.

Examples

>>> import matplotlib.pyplot as plt

>>> al = ok.AssetList(["SPY.US", "BND.US"], ccy="USD") >>> al.assets_close_monthly.plot() >>> plt.show()

- property assets_ror

Rate of return monthly time series for all assets.

- Returns:

- DataFrame

Rate of return monthly data.

- property currency

Return the base currency.

Such properties as rate of return and risk are adjusted to the base currency.

- Returns:

- str

Base currency.

- percentile_cagr(years, percentiles=[10, 50, 90])

Calculate given percentiles for portfolio rolling CAGR distribution from the historical data.

CAGR - Compound Annual Growth Rate. Each percentile is calculated for a period range from 1 year to ‘years’.

- Parameters:

- yearsint

Max window size for rolling CAGR in the distribution in years. It should not exceed 1/2 of the portfolio history period length ‘period_length’.

- percentileslist of int, default [10, 50, 90]

List of percentiles to be calculated.

- Returns:

- DataFrame

Table with percentiles values for each period from 1 to ‘years’.

Examples

>>> pf = ok.Portfolio( ... ["SPY.US", "AGG.US", "GLD.US"], ... weights=[0.60, 0.35, 0.05], ... rebalancing_strategy=ok.Rebalance(period="none"), ... ) >>> pf.percentile_cagr(years=5, percentiles=[1, 50, 99]) 1 50 99 years 1 -0.231327 0.098693 0.295343 2 -0.101689 0.091824 0.206471 3 -0.036771 0.085428 0.157833 4 -0.007674 0.085178 0.142195 5 0.030933 0.082865 0.134496

- plot_assets(kind='mean', tickers='tickers', pct_values=False, xy_text=(0, 10), **kwargs)

Plot asset points on the risk-return chart with annotations.

Annualized values for risk and return are used. Risk is the standard deviation of monthly rate of return time series. Return can be an annualized mean return (expected return) or CAGR (compound annual growth rate).

- Parameters:

- kind{‘mean’, ‘cagr’}, default ‘mean’

Type of return: annualized mean return (expected return) or CAGR (compound annual growth rate).

- tickers{‘tickers’, ‘names’, ‘local_names’} or list of str, default ‘tickers’

Annotation type for assets.

‘tickers’: asset symbols are shown in the form ‘SPY.US’.

‘names’: asset names are shown (for example, ‘SPDR S&P 500 ETF Trust’).

‘local_names’: native-language names (e.g. ‘Сбербанк’ / ‘贵州茅台’).

list of str: custom annotations for each asset.

Note

Rendering native (‘local_names’) labels written in CJK scripts (Chinese, Japanese, Korean) requires a CJK-capable matplotlib font; with the default fonts such glyphs appear as tofu boxes.

- pct_valuesbool, default False

If True, show risk and return values in percent. If False, show values as decimals.

- xy_texttuple, default (0, 10)

The shift of the annotation text (x, y) from the point.

- **kwargs

Arbitrary keyword arguments passed to matplotlib.pyplot.scatter.

- Returns:

- Axes

Matplotlib axes object.

Examples

>>> import matplotlib.pyplot as plt

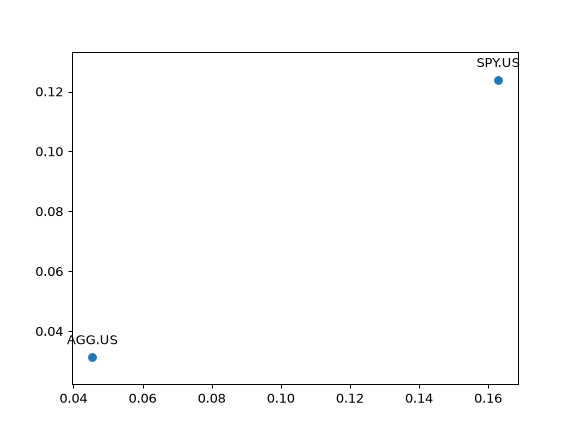

>>> al = ok.AssetList(["SPY.US", "AGG.US"], ccy="USD", inflation=False) >>> al.plot_assets() >>> plt.show()

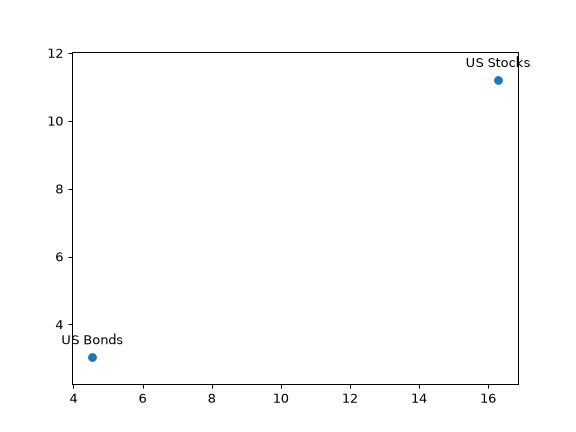

Plotting with default parameters values shows expected return, ticker annotations and algebraic values for risk and return. To use CAGR instead of expected return use kind=’cagr’.

>>> al.plot_assets( ... kind="cagr", ... tickers=["US Stocks", "US Bonds"], # use custom annotations for the assets ... pct_values=True, # risk and return values are in percents ... ) >>> plt.show()

- property symbols

Return a list of used financial symbols.

Symbols are similar to tickers but have a namespace information:

SPY.US is a symbol

SPY is a ticker

- Returns:

- list of str

List of used symbols.

- property tickers

Return a list of used tickers (symbols without a namespace).

Tickers are similar to symbols but do not have namespace information:

SPY is a ticker

SPY.US is a symbol

- Returns:

- list of str

List of used tickers.

- get_sharpe_ratio(rf_return=0)

Calculate Sharpe ratio.

The Sharpe ratio is the average annual return in excess of the risk-free rate per unit of risk (annualized standard deviation).

Risk-free rate should be taken according to the Portfolio base currency.

- Parameters:

- rf_returnfloat, default 0

Risk-free rate of return.

- Returns:

- float

Examples

>>> pf = ok.Portfolio(["VOO.US", "BND.US"], weights=[0.40, 0.60]) >>> pf.get_sharpe_ratio(rf_return=0.04) 0.7412193684695373

- get_sortino_ratio(t_return=0)

Calculate Sortino ratio for the portfolio with specified target return.

Sortion ratio measures the risk-adjusted return of portfolio. It is a modification of the Sharpe ratio but penalizes only those returns falling below a specified target rate of return, while the Sharpe ratio penalizes both upside and downside volatility equally.

- Parameters:

- t_returnfloat, default 0

Traget rate of return.

- Returns:

- float

Examples

>>> pf = ok.Portfolio(["VOO.US", "BND.US"], last_date="2021-12") >>> pf.get_sortino_ratio(t_return=0.02) 1.4377728903230174

- tracking_error(benchmark, rolling_window=None, method='rms')

Calculate ex-post tracking error time series of the portfolio against a benchmark.

Tracking error is an ex-post (backward-looking) measure of how closely the portfolio follows the benchmark. It is computed from the realized monthly return differences between the portfolio and the benchmark, and is annualized (multiplied by sqrt(12)). Tracking error values are decimal fractions: 0.05 corresponds to 5% annualized.

Two formulas are available (method parameter):

“rms” (default): root-mean-square of the return differences. The differences are not centered around their mean, hence the systematic lag between the portfolio and the benchmark (tracking difference) is included in the result.

“std”: sample standard deviation of the return differences with Bessel’s correction — the classic tracking error definition (Hwang & Satchell, “Tracking Error: Ex-Ante versus Ex-Post Measures”, 2001, eq. 2) measuring the pure volatility of deviations from the benchmark. The first point of the expanding time series is dropped (a single observation has no standard deviation).

The benchmark rate of return is converted to the portfolio base currency, and the time period is limited to the intersection of the portfolio and benchmark available histories.

- Parameters:

- benchmarkstr, Asset, Portfolio

Benchmark ticker (e.g. “SP500TR.INDX”) or an asset-like object (Asset, Portfolio).

- rolling_windowint or None, default None

Size of the moving window in months. Must be at least 12 months. If None calculate expanding tracking error.

- method{“rms”, “std”}, default “rms”

Tracking error formula: “rms” for the uncentered root-mean-square of return differences, “std” for the centered sample standard deviation.

- Returns:

- Series

Expanding or rolling annualized tracking error time series. The series is named after the portfolio symbol.

Examples

>>> import matplotlib.pyplot as plt

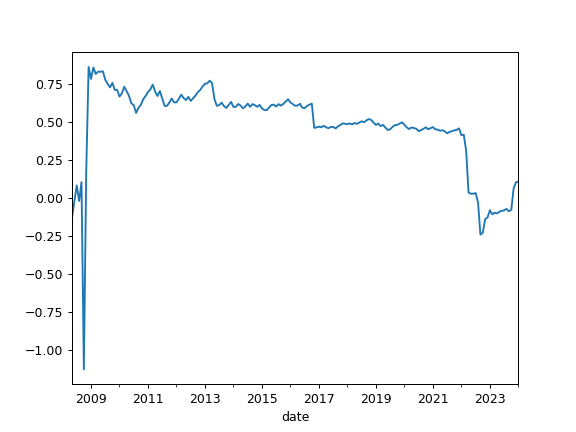

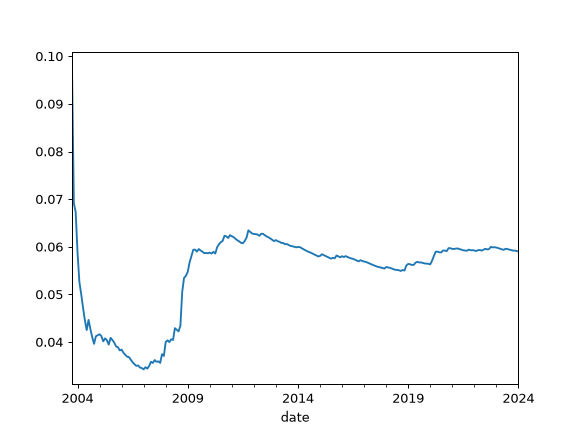

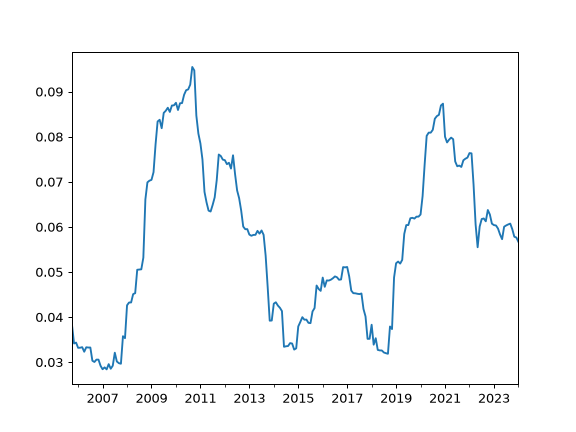

>>> pf = ok.Portfolio(["SPY.US", "AGG.US"], weights=[0.60, 0.40], last_date="2024-01") >>> pf.tracking_error(benchmark="SP500TR.INDX").plot() >>> plt.show()

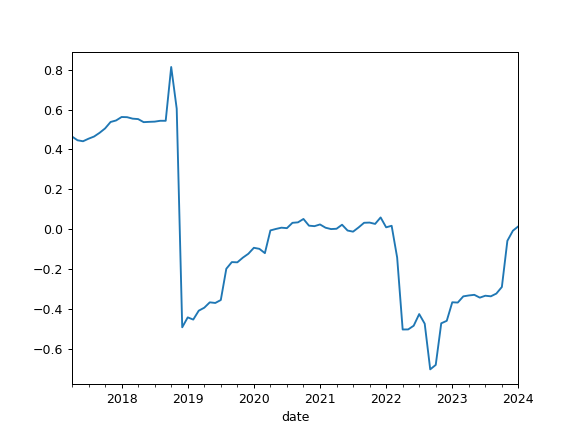

To calculate rolling tracking error set rolling_window to a number of months (moving window size):

>>> pf.tracking_error(benchmark="SP500TR.INDX", rolling_window=24, method="std").plot() >>> plt.show()

- property diversification_ratio

Calculate Diversification Ratio for the portfolio.

The Diversification Ratio is the ratio of the weighted average of assets risks divided by the portfolio risk. In this case risk is the annuilized standatd deviation for the rate of return .

- Returns:

- float

Examples

>>> pf = ok.Portfolio(["VOO.US", "BND.US"], weights=[0.7, 0.3], last_date="2021-12") >>> pf.diversification_ratio 1.1264305597257505

- property okamaio_link

URL link to portfolio at okama.io.

Portfolio with the same tickers, weights and other properties at okama.io financial widgets.

- Returns:

- str

URL link to portfolio at okama.io.

Examples

>>> pf = ok.Portfolio( ... ["SPY.US", "AGG.US"], ... weights=[0.60, 0.40], ... rebalancing_strategy=ok.Rebalance(period="year", abs_deviation=0.05), ... ) >>> pf.okamaio_link 'https://okama.io/portfolio?tickers=SPY.US,AGG.US&ccy=USD&first_date=2003-10&last_date=2024-08&weights=60,40&rebal=year&abs_dev=5&symbol=portfolio_6323.PF'