Okama Documentation

okama is a Python library for investment portfolio analysis and optimization. It applies concepts commonly used in quantitative finance.

okama provides access to free end-of-day historical market data and macroeconomic indicators through an API.

…entities should not be multiplied without necessity

– William of Ockham (c. 1287–1347)

Okama main features

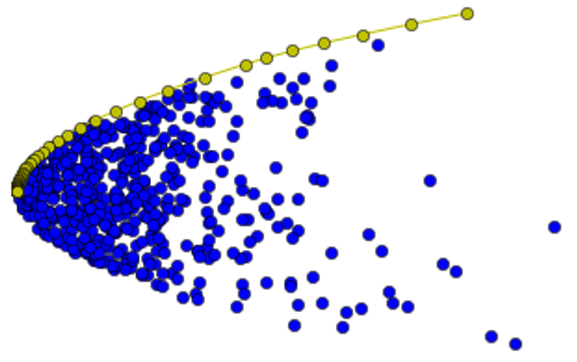

Constrained Markowitz Mean-Variance Analysis (MVA) and portfolio optimization

Multi-period Efficient Frontier optimization with rebalancing constraints

Investment portfolios with contribution and withdrawal cash flows (DCF)

Monte Carlo simulations for financial assets and investment portfolios

Popular risk metrics: VaR, CVaR, semideviation, variance, and drawdowns

Forecasting models based on normal, lognormal, and Student’s t distributions

Distribution fitting and goodness-of-fit testing on historical data

Dividend yield and other dividend indicators for stocks

Backtesting and comparing the historical performance of a broad range of assets and indexes in multiple currencies

Methods for tracking the performance of index funds (ETFs) and comparing them with benchmarks

Main macroeconomic indicators: inflation, central bank rates, and financial ratios

Matplotlib visualizations for the Efficient Frontier, Transition Map, and asset risk/return performance

Financial data and macroeconomic indicators

okama can work with free financial data available through its API.

End of day historical data

Stocks and ETFs for major world markets

Mutual funds

Commodities

Currencies

Stock indexes

Macroeconomic indicators

For several countries, including the USA, the United Kingdom, the European Union, Russia, and Israel:

Inflation

Central bank rates

CAPE10 (Shiller P/E), or cyclically adjusted price-to-earnings ratios

Other historical data

Real estate prices

Top bank rates

Installation

Okama can be installed from PyPI:

pip install okama

The latest development version can be installed directly from GitHub:

git clone https://github.com/mbk-dev/okama@dev

poetry install

Warning

The development version of okama may have technical and financial issues. Use it carefully and at your own risk.

Quick Start

Index Funds Performance

Main

Assets & Portfolio

|

A financial asset, that could be used in a list of assets or in portfolio. |

|

List of financial assets. |

|

Investment portfolio. |

|

Rebalancing strategy for an investment portfolio. |

Cash Flows & DCF

|

Discounted cash flow (DCF) methods for a Portfolio. |

|

Monte Carlo simulation parameters for an investment portfolio. |

|

Cash flow strategy with regular indexed withdrawals or contributions. |

|

Cash flow strategy with regular fixed percentage withdrawals or contributions. |

|

Cash flow strategy with user-defined withdrawals and contributions. |

|

Vanguard Dynamic Spending strategy. |

|

Withdrawal strategy that reduces the withdrawal amount if the portfolio drawdown exceeds a certain threshold. |

Efficient Frontier

|

Efficient Frontier with multi-period optimization. |

Macroeconomics

|

Inflation related data and methods. |

|

Rates of central banks and banks. |

|

Macroeconomic indicators and ratios. |

Data Access & Search

okama.search()Search symbols by ticker, name, or ISIN.

okama.symbols_in_namespace()Return all symbols available in a namespace.

okama.namespacesReturns a dictionary of available data namespaces and their descriptions.