![]()

You can run the code examples in Google Colab.

To install the package:

[5]:

%%capture --no-stderr

%pip install --quiet -U okama

Import okama and matplotlib packages.

[ ]:

import warnings

import matplotlib.pyplot as plt

import okama as ok

warnings.filterwarnings("ignore")

plt.rcParams["figure.figsize"] = [12.0, 6.0]

Get information about a single asset

You can start by getting general information about a single asset or index.

[7]:

one_asset = ok.Asset("VOO.US")

one_asset

[7]:

symbol VOO.US

name Vanguard S&P 500 ETF

country USA

exchange NYSE ARCA

currency USD

type ETF

isin US9229083632

first date 2010-10

last date 2026-03

period length 15.40

dtype: object

[8]:

# live (20 min delay) price

one_asset.price

[8]:

580.93

[9]:

# dividends history

one_asset.dividends.tail(10)

[9]:

date

2025-06 1.7447

2025-07 0.0000

2025-08 0.0000

2025-09 1.7400

2025-10 0.0000

2025-11 0.0000

2025-12 1.7710

2026-01 0.0000

2026-02 0.0000

2026-03 1.8724

Freq: M, Name: VOO.US, dtype: float64

Financial Database: Tickers & Namespaces

If you are unsure whether a ticker is available or how an asset is named, check it with search:

[10]:

ok.search("exxon")

[10]:

| symbol | ticker | name | country | exchange | currency | type | isin | |

|---|---|---|---|---|---|---|---|---|

| 0 | XOM.US | XOM | Exxon Mobil Corp | USA | NYSE | USD | Common Stock | US30231G1022 |

| 1 | XONA.XETR | XONA | Exxon Mobil Corporation | Germany | XETR | EUR | Common Stock | US30231G1022 |

| 2 | 0R1M.LSE | 0R1M | Exxon Mobil Corporation | UK | LSE | USD | Common Stock | US30231G1022 |

| 3 | XO3S.LSE | XO3S | Leverage Shares -3x Short Exxon (XOM) ETP Secu... | UK | LSE | USD | ETF | |

| 4 | XONA.XFRA | XONA | Exxon Mobil Corporation | Germany | XFRA | EUR | Common Stock | US30231G1022 |

| 5 | XONA.XSTU | XONA | EXXON MOBIL (XONA.SG) | Germany | XSTU | EUR | Common Stock | US30231G1022 |

A namespace is the set of characters after the period in a ticker (SPY.US).

Namespaces are based on MICs (Market Identifier Codes) and okama’s own codes for macroeconomic parameters.

[11]:

# available namespaces

ok.namespaces

[11]:

{'CBR': 'Central Banks official currency exchange rates',

'CC': 'Cryptocurrency pairs with USD',

'COMM': 'Commodities prices',

'FX': 'FOREX currency market',

'INDX': 'Indexes',

'INFL': 'Inflation',

'LSE': 'London Stock Exchange',

'MOEX': 'Moscow Exchange',

'PF': 'Investment Portfolios',

'PIF': 'Russian open-end mutual funds',

'RATE': 'Bank deposit rates',

'RATIO': 'Financial ratios',

'RE': 'Real estate prices',

'US': 'US Stock Exchanges and mutual funds',

'XAMS': 'Euronext Amsterdam',

'XETR': 'XETRA Exchange',

'XFRA': 'Frankfurt Stock Exchange',

'XSTU': 'Stuttgart Exchange',

'XTAE': 'Tel Aviv Stock Exchange (TASE)'}

[12]:

# available symbols in namespace

ok.symbols_in_namespace("INDX")

[12]:

| symbol | ticker | name | country | exchange | currency | type | isin | |

|---|---|---|---|---|---|---|---|---|

| 0 | 000906.INDX | 000906 | China Securities 800 | Unknown | INDX | CNY | INDEX | |

| 1 | 0O7N.INDX | 0O7N | Scale All Share GR EUR | Germany | INDX | EUR | INDEX | |

| 2 | 3LHE.INDX | 3LHE | ESTX 50 Corporate Bond TR | Greece | INDX | EUR | INDEX | |

| 3 | 5SP2550.INDX | 5SP2550 | S&P 500 Retailing (Industry Group) | USA | INDX | USD | INDEX | |

| 4 | 990100.INDX | 990100 | MSCI International World Index Price | Unknown | INDX | USD | INDEX | |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2380 | XUSIN.INDX | XUSIN | BIST Industrials | Turkey | INDX | TRY | INDEX | |

| 2381 | XUSRD.INDX | XUSRD | BIST Sustainability | Turkey | INDEX | TRY | INDEX | |

| 2382 | XUTEK.INDX | XUTEK | BIST Technology | Turkey | INDEX | TRY | INDEX | |

| 2383 | YMU0.INDX | YMU0 | E-mini Dow $5 Future Sept 20 | USA | INDX | USD | Futures | |

| 2384 | YY1P.INDX | YY1P | EURO STOXX SMALL | USA | INDX | EUR | INDEX | CH0009107456 |

2385 rows × 8 columns

Compare assets from different stock markets

AssetList is used to compare different types of stocks, indexes, currencies, or commodities. Asset performance is adjusted to the base currency (USD by default).

[13]:

ls = ["SPY.US", "BND.US", "GC.COMM", "EUR.FX"]

currency = "EUR" # base currency

[14]:

x = ok.AssetList(

ls, ccy=currency, last_date="2020-01"

) # first_date and last_date limits the Rate of Return time series

x

[14]:

assets [SPY.US, BND.US, GC.COMM, EUR.FX]

currency EUR

first_date 2007-05

last_date 2020-01

period_length 12 years, 9 months

inflation EUR.INFL

dtype: object

[15]:

x.names

[15]:

{'SPY.US': 'SPDR S&P 500 ETF Trust',

'BND.US': 'Vanguard Total Bond Market Index Fund ETF Shares',

'GC.COMM': 'Gold (COMEX)',

'EUR.FX': 'US Dollar/Euro FX Cross Rate'}

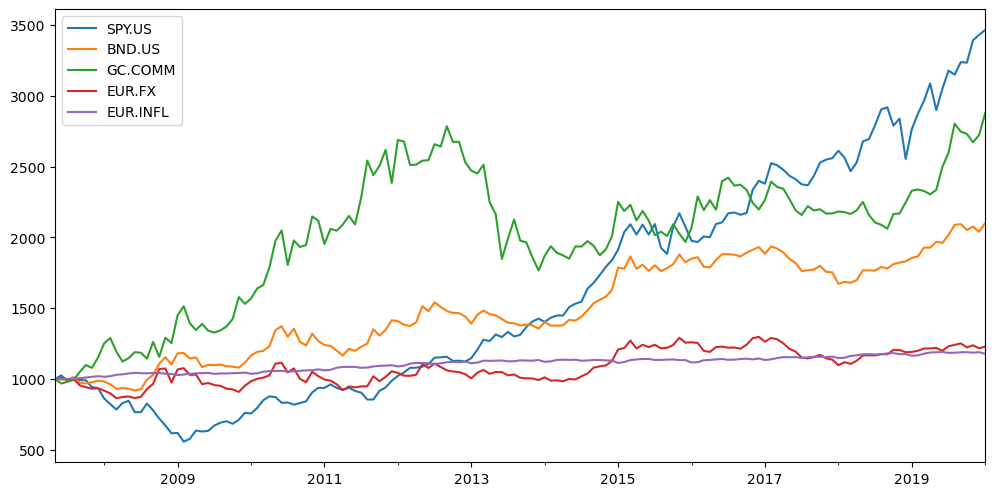

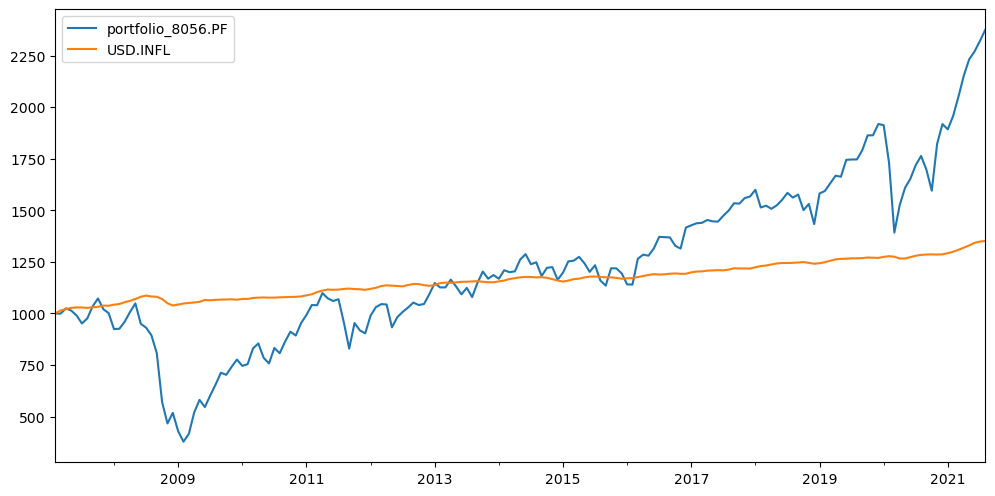

Let’s look at the accumulated return and compare it with inflation.

[16]:

x.wealth_indexes.plot();

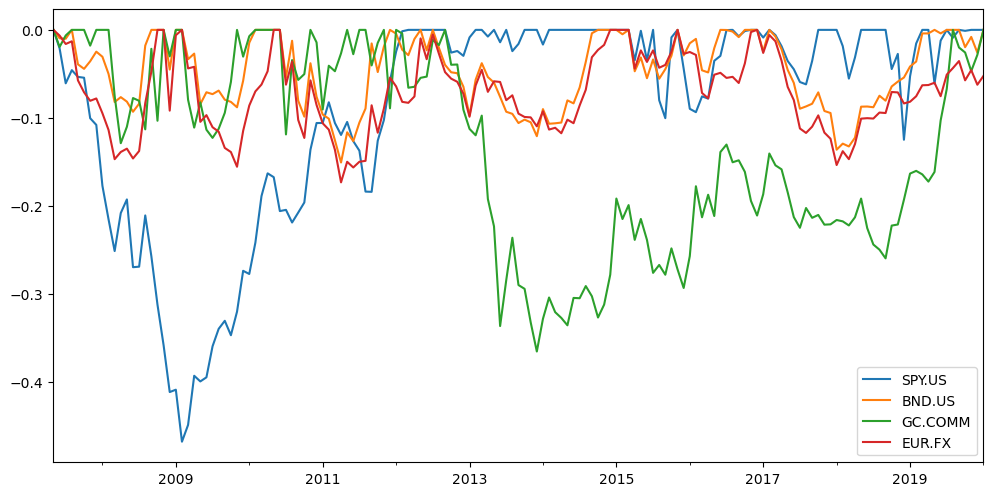

Drawdown history is also easy to inspect.

[17]:

x.drawdowns.plot();

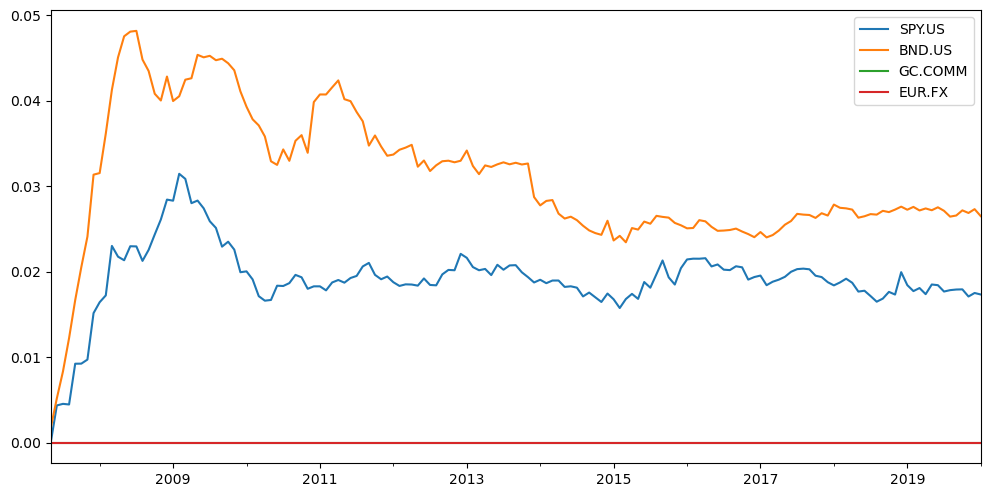

See the dividend yield history for all the assets in the list.

[18]:

x.dividend_yield.tail()

[18]:

| SPY.US | BND.US | GC.COMM | EUR.FX | |

|---|---|---|---|---|

| 2019-09 | 0.017978 | 0.026646 | 0.0 | 0.0 |

| 2019-10 | 0.017931 | 0.027154 | 0.0 | 0.0 |

| 2019-11 | 0.017083 | 0.026846 | 0.0 | 0.0 |

| 2019-12 | 0.017482 | 0.027272 | 0.0 | 0.0 |

| 2020-01 | 0.017219 | 0.026330 | 0.0 | 0.0 |

… or plot the same results.

[19]:

x.dividend_yield.plot();

The .describe() method shows the main parameters (risk metrics, rates of return, etc.) for the list of assets.

[20]:

x.describe(years=[1, 10]) # You can specify the period or leave the default: 1, 5 and 10 years

[20]:

| property | period | SPY.US | BND.US | GC.COMM | EUR.FX | inflation | |

|---|---|---|---|---|---|---|---|

| 0 | Compound return | YTD | 0.015294 | 0.035811 | 0.058055 | 0.0107 | -0.01 |

| 1 | CAGR | 1 years | 0.264954 | 0.143258 | 0.249053 | 0.031992 | 0.011915 |

| 2 | CAGR | 10 years | 0.164899 | 0.061206 | 0.062743 | 0.022543 | 0.012802 |

| 3 | CAGR | 12 years, 9 months | 0.102941 | 0.060522 | 0.086488 | 0.016364 | 0.01294 |

| 4 | Annualized mean return | 12 years, 9 months | 0.107585 | 0.063661 | 0.098019 | 0.021451 | NaN |

| 5 | Dividend yield | LTM | 0.017219 | 0.02633 | 0.0 | 0.0 | NaN |

| 6 | Risk | 12 years, 9 months | 0.150425 | 0.10467 | 0.19155 | 0.105235 | NaN |

| 7 | CVAR | 12 years, 9 months | 0.330952 | 0.128223 | 0.3078 | 0.155073 | NaN |

| 8 | Max drawdowns | 12 years, 9 months | -0.468342 | -0.153572 | -0.368852 | -0.173337 | NaN |

| 9 | Max drawdowns dates | 12 years, 9 months | 2009-02 | 2011-04 | 2013-12 | 2011-04 | NaN |

| 10 | Inception date | None | 1993-02 | 2007-05 | 1975-02 | 1975-02 | 1996-02 |

| 11 | Last asset date | None | 2020-01 | 2020-01 | 2020-01 | 2020-01 | 2020-01 |

| 12 | Common last data date | None | 2020-01 | 2020-01 | 2020-01 | 2020-01 | 2020-01 |

Correlation Matrix

If you need to check the correlation (or covariance) between asset returns, you can use native pandas functions.

Monthly rate-of-return time series are available through the .assets_ror property:

[21]:

x.assets_ror.tail()

[21]:

| Symbols | SPY.US | BND.US | GC.COMM | EUR.FX |

|---|---|---|---|---|

| date | ||||

| 2019-09 | 0.030714 | 0.005237 | -0.024587 | 0.0084 |

| 2019-10 | 0.002680 | -0.015959 | 0.011607 | -0.0227 |

| 2019-11 | 0.049567 | 0.012495 | -0.017791 | 0.0123 |

| 2019-12 | 0.011605 | -0.017688 | 0.019174 | -0.0174 |

| 2020-01 | 0.015294 | 0.035811 | 0.058055 | 0.0107 |

The correlation matrix can be obtained with x.assets_ror.corr().

[22]:

x.assets_ror.corr()

[22]:

| Symbols | SPY.US | BND.US | GC.COMM | EUR.FX |

|---|---|---|---|---|

| Symbols | ||||

| SPY.US | 1.000000 | 0.179704 | -0.085518 | 0.211607 |

| BND.US | 0.179704 | 1.000000 | 0.338168 | 0.907689 |

| GC.COMM | -0.085518 | 0.338168 | 1.000000 | 0.185743 |

| EUR.FX | 0.211607 | 0.907689 | 0.185743 | 1.000000 |

Covariance matrix:

[23]:

x.assets_ror.cov()

[23]:

| Symbols | SPY.US | BND.US | GC.COMM | EUR.FX |

|---|---|---|---|---|

| Symbols | ||||

| SPY.US | 0.001537 | 0.000200 | -0.000168 | 0.000246 |

| BND.US | 0.000200 | 0.000809 | 0.000483 | 0.000767 |

| GC.COMM | -0.000168 | 0.000483 | 0.002522 | 0.000277 |

| EUR.FX | 0.000246 | 0.000767 | 0.000277 | 0.000883 |

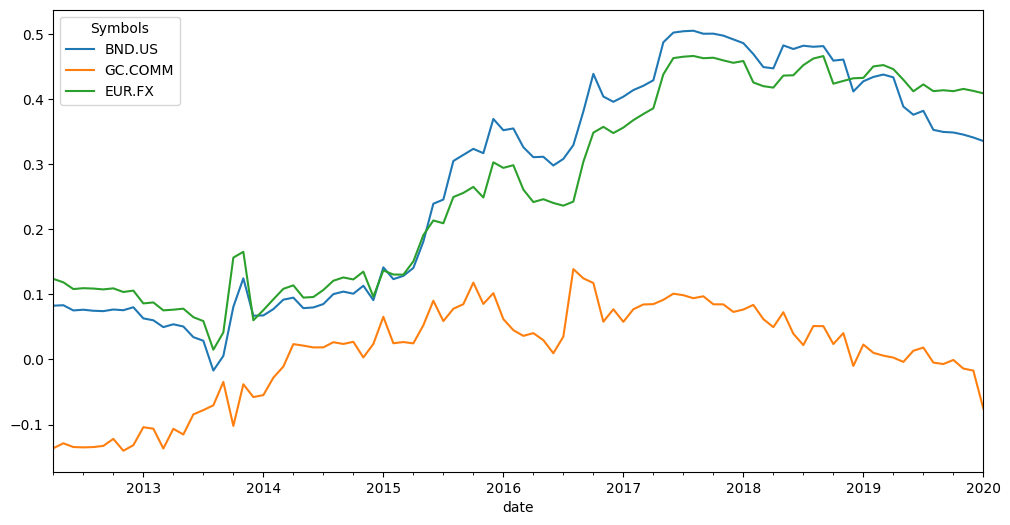

AssetList (SPY.US in this example).[24]:

x.index_corr(rolling_window=12 * 5).plot();

Basic portfolio methods

Let’s create a portfolio with three assets and USD as the base currency. We need to specify the weights.

[25]:

tickers = [

"VNQ.US",

"DBXD.XFRA",

"MCFTR.INDX",

] # we can create lists of assets and portfolio containing general type of assets and **indexes**

w = [0.5, 0.25, 0.25]

currency = "USD"

[26]:

y = ok.Portfolio(tickers, ccy=currency, weights=w)

y

[26]:

symbol portfolio_2745.PF

assets [VNQ.US, DBXD.XFRA, MCFTR.INDX]

weights [0.5, 0.25, 0.25]

rebalancing_period month

rebalancing_abs_deviation None

rebalancing_rel_deviation None

currency USD

inflation USD.INFL

first_date 2007-02

last_date 2026-02

period_length 19 years, 1 months

dtype: object

[27]:

y.table

[27]:

| asset name | ticker | weights | |

|---|---|---|---|

| 0 | Vanguard Real Estate Index Fund ETF Shares | VNQ.US | 0.50 |

| 1 | Xtrackers - DAX UCITS ETF | DBXD.XFRA | 0.25 |

| 2 | MOEX Russia Total Return Index | MCFTR.INDX | 0.25 |

A portfolio has the same .wealth_index property (accumulated return) as an AssetList object.

[28]:

y.wealth_index.plot();

Risk metrics

You can use risk metrics such as volatility (standard deviation), semideviation, max drawdown, VaR, and CVaR.

[29]:

y.risk_annual.tail()

[29]:

date

2025-10 0.219978

2025-11 0.219891

2025-12 0.219411

2026-01 0.219229

2026-02 0.219067

Freq: M, Name: portfolio_2745.PF, dtype: float64

[30]:

y.semideviation_annual

[30]:

np.float64(0.17009760627025125)

[31]:

y.get_var_historic(level=1)

[31]:

np.float64(0.5422501601074122)

[32]:

y.get_cvar_historic(level=5)

[32]:

np.float64(0.46925923391795993)

[33]:

y.drawdowns.min()

[33]:

np.float64(-0.648114355818486)

.recovery_period.[34]:

y.recovery_period.max() / 12 # years

[34]:

np.float64(3.4166666666666665)

.describe() shows the main portfolio properties for different trailing periods.

[35]:

y.describe()

[35]:

| property | period | portfolio_2745.PF | inflation | |

|---|---|---|---|---|

| 0 | compound return | YTD | 0.059764 | 0.008417 |

| 1 | CAGR | 1 years | 0.116881 | 0.024041 |

| 2 | CAGR | 5 years | 0.080232 | 0.044380 |

| 3 | CAGR | 10 years | 0.097082 | 0.032603 |

| 4 | CAGR | 19 years, 1 months | 0.05701 | 0.025419 |

| 5 | Annualized mean return | 19 years, 1 months | 0.076655 | NaN |

| 6 | Dividend yield | LTM | 0.018141 | NaN |

| 7 | Risk | 19 years, 1 months | 0.219067 | NaN |

| 8 | CVAR (α=1) | 19 years, 1 months | 0.567506 | NaN |

| 9 | Max drawdown | 19 years, 1 months | -0.648114 | NaN |

| 10 | Max drawdown date | 19 years, 1 months | 2009-02 | NaN |