![]()

You can run the code examples in Google Colab.

To install the package:

[ ]:

%%capture --no-stderr

%pip install --quiet -U okama

import okama and matplotlib packages …

[1]:

import warnings

import matplotlib.pyplot as plt

import okama as ok

warnings.simplefilter(action="ignore", category=FutureWarning)

plt.rcParams["figure.figsize"] = [12.0, 6.0]

Portfolio and AssetList are helpful for studying portfolio properties and comparing portfolios with each other. With AssetList, we can even compare a portfolio with stocks, indexes, and other financial assets, because a portfolio is just a special case of a financial asset.

In this tutorial we will learn how to:

create an investment portfolio and inspect its basic properties

understand rebalancing strategies and asset allocation

measure portfolio risk

analyze accumulated return, CAGR, and dividend yield

compare several portfolios

forecast portfolio performance

Create an investment portfolio

Portfolios are quite similar to AssetList, but we need to specify weights and a rebalancing strategy.

All arguments have default values and can be omitted.

[2]:

basic_portfolio = ok.Portfolio()

basic_portfolio

[2]:

symbol portfolio_4992.PF

assets [SPY.US]

weights [1.0]

rebalancing_period month

rebalancing_abs_deviation None

rebalancing_rel_deviation None

currency USD

inflation USD.INFL

first_date 1993-02

last_date 2025-09

period_length 32 years, 8 months

dtype: object

SPY.US.USD.inflation=True.Rebalancing is the process by which an investor restores a portfolio to its target allocation by selling and buying assets. After rebalancing, all assets return to their original weights.

In the rebalancing strategy, the period can be: month, year, half-year, quarter, or none (for portfolios without rebalancing).

[3]:

rf3 = ok.Portfolio(

["BND.US", "VTI.US", "VXUS.US"],

weights=[0.40, 0.40, 0.20],

rebalancing_strategy=ok.Rebalance(period="year"), # set the rebalancing period

)

rf3

[3]:

symbol portfolio_9868.PF

assets [BND.US, VTI.US, VXUS.US]

weights [0.4, 0.4, 0.2]

rebalancing_period year

rebalancing_abs_deviation None

rebalancing_rel_deviation None

currency USD

inflation USD.INFL

first_date 2011-02

last_date 2025-09

period_length 14 years, 8 months

dtype: object

.assets_first_dates and .assets_last_dates.[4]:

rf3.assets_first_dates

[4]:

{'USD': Timestamp('1913-02-01 00:00:00'),

'VTI.US': Timestamp('2001-06-01 00:00:00'),

'BND.US': Timestamp('2007-05-01 00:00:00'),

'VXUS.US': Timestamp('2011-02-01 00:00:00'),

'USD.INFL': Timestamp('1913-02-01 00:00:00')}

[5]:

rf3.newest_asset

[5]:

'VXUS.US'

Here, VXUS.US is the asset with the shortest history, so it limits the history available for the entire portfolio.

[6]:

rf3.assets_last_dates

[6]:

{'BND.US': Timestamp('2025-11-01 00:00:00'),

'VTI.US': Timestamp('2025-11-01 00:00:00'),

'VXUS.US': Timestamp('2025-11-01 00:00:00'),

'USD': Timestamp('2099-12-01 00:00:00'),

'USD.INFL': Timestamp('2025-09-01 00:00:00')}

Inflation can also limit the available history. If you want to include the latest month even when inflation data is not yet available, instantiate the portfolio with inflation=False.

symbol= when creating the portfolio or set it afterward:[7]:

rf3.symbol = "RF3_portfolio.PF" # 'PF' namespace is reserved for portfolios.

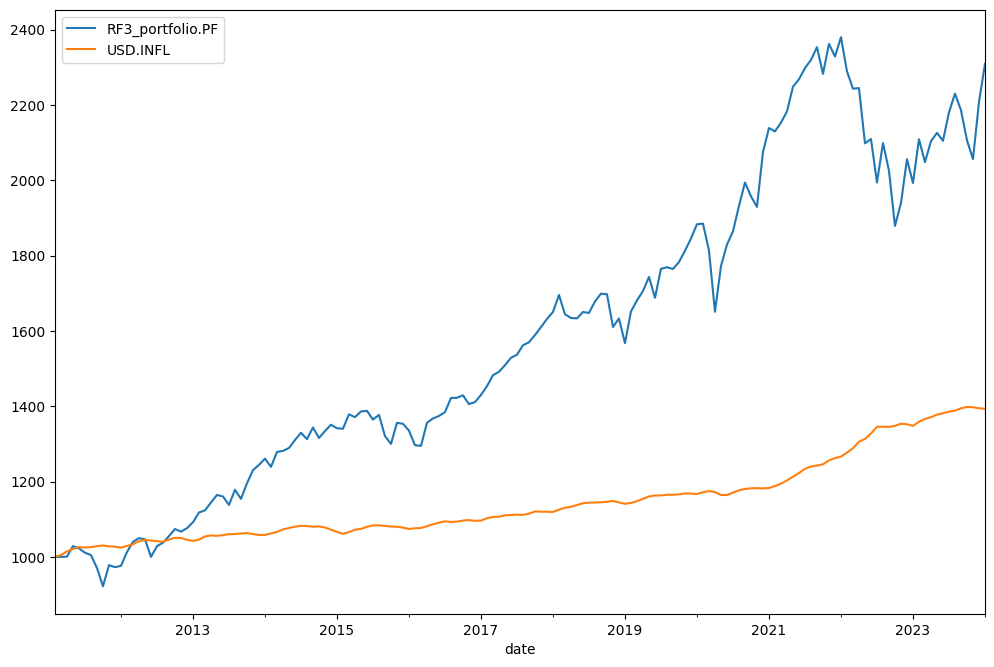

The wealth index (Cumulative Wealth Index) is a time series that shows the portfolio value over the historical period. The initial investment is 1,000 units of the base currency.

[8]:

rf3.wealth_index.plot();

Rebalancing strategy and asset allocation

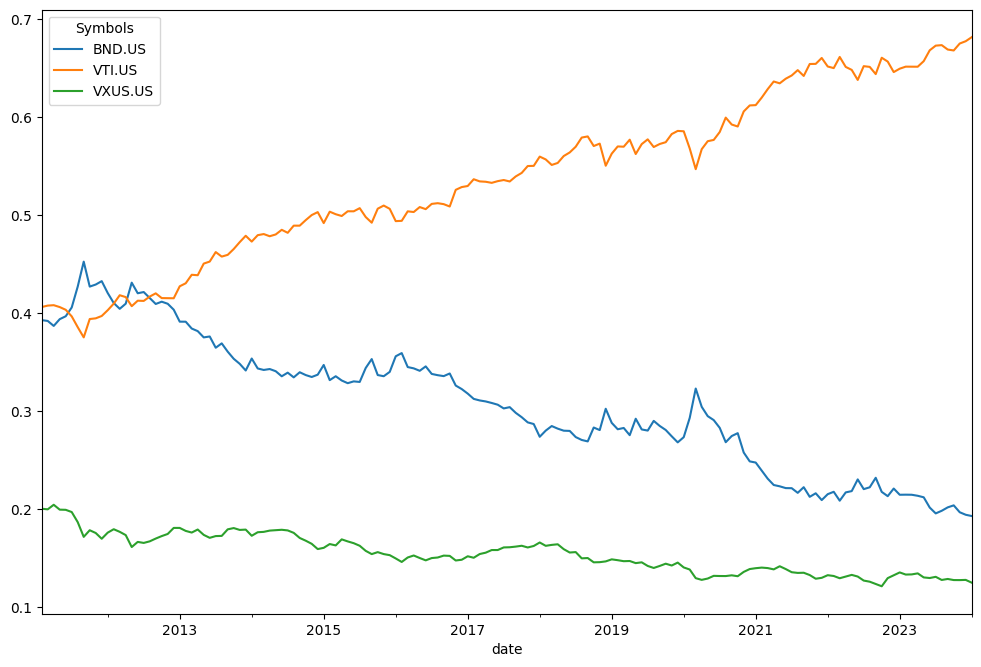

The original asset-allocation table is available through .table:

[9]:

rf3.table

[9]:

| asset name | ticker | weights | |

|---|---|---|---|

| 0 | Vanguard Total Bond Market Index Fund ETF Shares | BND.US | 0.4 |

| 1 | Vanguard Total Stock Market Index Fund ETF Shares | VTI.US | 0.4 |

| 2 | Vanguard Total International Stock Index Fund ... | VXUS.US | 0.2 |

.weights_ts:[10]:

rf3.weights_ts.plot();

Let’s create the same Rick Ferri portfolio, but without rebalancing. In that case, the asset allocation will drift and never return to the original weights.

[11]:

rf3_no_rebalancing = ok.Portfolio(

["BND.US", "VTI.US", "VXUS.US"],

weights=[0.40, 0.40, 0.20],

rebalancing_strategy=ok.Rebalance(period="none"),

)

Now it is easy to see how the weights drift over time, and the portfolio ends up overweight in stocks.

[12]:

rf3_no_rebalancing.weights_ts.plot();

Risk metrics of the portfolio

A portfolio has several methods for inspecting risk metrics. By default, risk means the standard deviation of the return time series:

risk_monthly(standard deviation of monthly returns)risk_annual(annualized standard deviation)semideviation_monthly(downside risk for monthly returns)semideviation_annual(annualized semideviation)get_var_historic(historical Value at Risk for the portfolio)get_cvar_historic(historical Conditional Value at Risk for the portfolio)drawdowns(percentage decline from a previous peak)recovery_period(the longest recovery period after a drawdown in portfolio value)

[13]:

rf3.risk_annual.tail() # aanualized values time series for standard deviation of return

[13]:

date

2025-05 0.100104

2025-06 0.100318

2025-07 0.100023

2025-08 0.099949

2025-09 0.099924

Freq: M, Name: RF3_portfolio.PF, dtype: float64

[14]:

rf3.semideviation_annual # annualized value for downside risk

[14]:

np.float64(0.07586435955895295)

[15]:

rf3.get_cvar_historic(time_frame=12, level=1) # one year CVAR with confidence level 1%

[15]:

np.float64(0.1779330903217476)

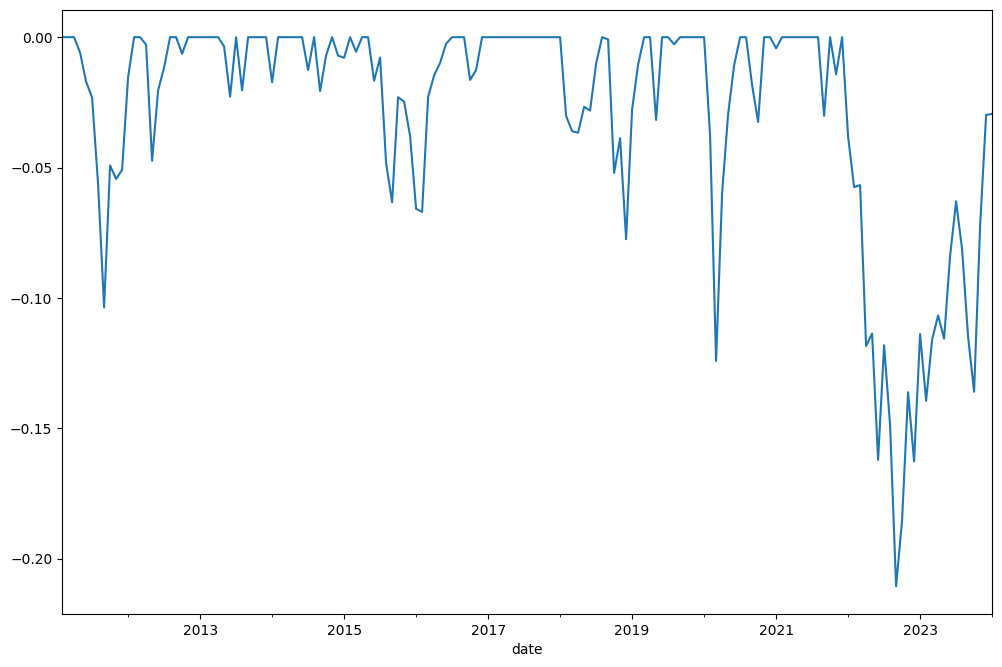

Drawdowns (the percent decline from a previous peak) are easy to plot …

[16]:

rf3.drawdowns.plot();

[17]:

rf3.drawdowns.nsmallest(5) # 5 Biggest drawdowns

[17]:

date

2022-09 -0.210563

2022-10 -0.185137

2022-12 -0.162683

2022-06 -0.162101

2022-08 -0.148924

Freq: M, Name: RF3_portfolio.PF, dtype: float64

recovery_period is closely related to drawdowns. It shows the longest recovery period for the portfolio value after a drawdown.

[18]:

rf3.recovery_period.nlargest() / 12 # we want it in years

[18]:

date

2024-02 2.166667

2016-06 1.083333

2012-01 0.750000

2018-07 0.500000

2019-02 0.500000

Freq: M, Name: RF3_portfolio.PF, dtype: float64

Accumulated return, CAGR and dividend yield

A portfolio has several metrics that can be used to measure returns and income:

wealth_index(the value of the portfolio over the historical period)wealth_index_with_assets(wealth index together with underlying asset values)mean_return_monthly(arithmetic mean of the portfolio return)mean_return_annual(annualized value of the monthly mean)annual_return_ts(calendar-year return time series)get_cagr(Compound Annual Growth Rate for a given trailing period)get_rolling_cagr(rolling CAGR)get_cumulative_return(expanding cumulative return time series over a given trailing period)get_rolling_cumulative_return(rolling cumulative return)dividend_yield(portfolio LTM dividend-yield monthly time series)

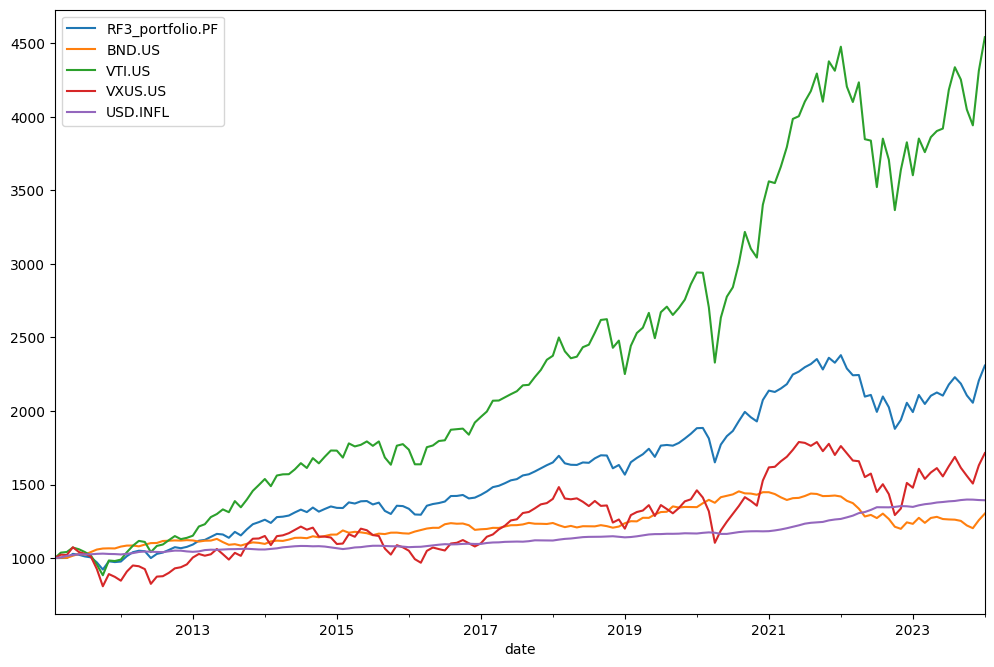

The wealth index is the simplest time series for showing portfolio value growth (we have already seen it above). Sometimes it is useful to compare portfolio growth with the growth of the underlying assets. For that, use wealth_index_with_assets.

[19]:

rf3.wealth_index_with_assets.plot();

The mean portfolio return can be annualized from the monthly mean:

[20]:

rf3.mean_return_annual

[20]:

np.float64(0.07778090663476697)

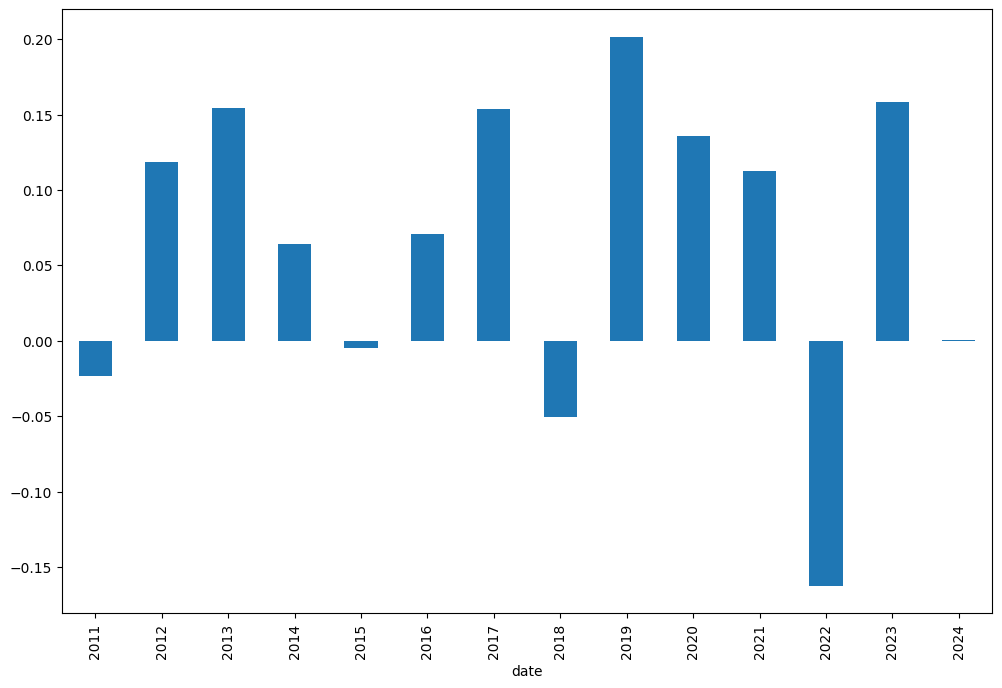

It is always useful to see how the portfolio performed on a calendar-year basis. The annual return time series shows the portfolio return for each year:

[24]:

rf3.annual_return_ts(return_type="cagr").tail() # can be cagr or arithmetic_mean

[24]:

date

2021 0.112746

2022 -0.162683

2023 0.158682

2024 0.110973

2025 0.134785

Freq: Y-DEC, Name: RF3_portfolio.PF, dtype: float64

… or as a bar chart:

[26]:

rf3.annual_return_ts(return_type="cagr").plot(kind="bar");

One of the most important return metrics is CAGR (Compound Annual Growth Rate). It can be seen for trailing periods (parameter period is in years):

[27]:

rf3.get_cagr(period=5) # portfolio is initiated with inflation=True. Hence, we see CAGR with mean inflation.

[27]:

RF3_portfolio.PF 0.082588

USD.INFL 0.045298

dtype: float64

[28]:

rf3.get_cagr(period=5, real=True) # when real=True CAGR is adjusted for inflation (real CAGR)

[28]:

RF3_portfolio.PF 0.035674

dtype: float64

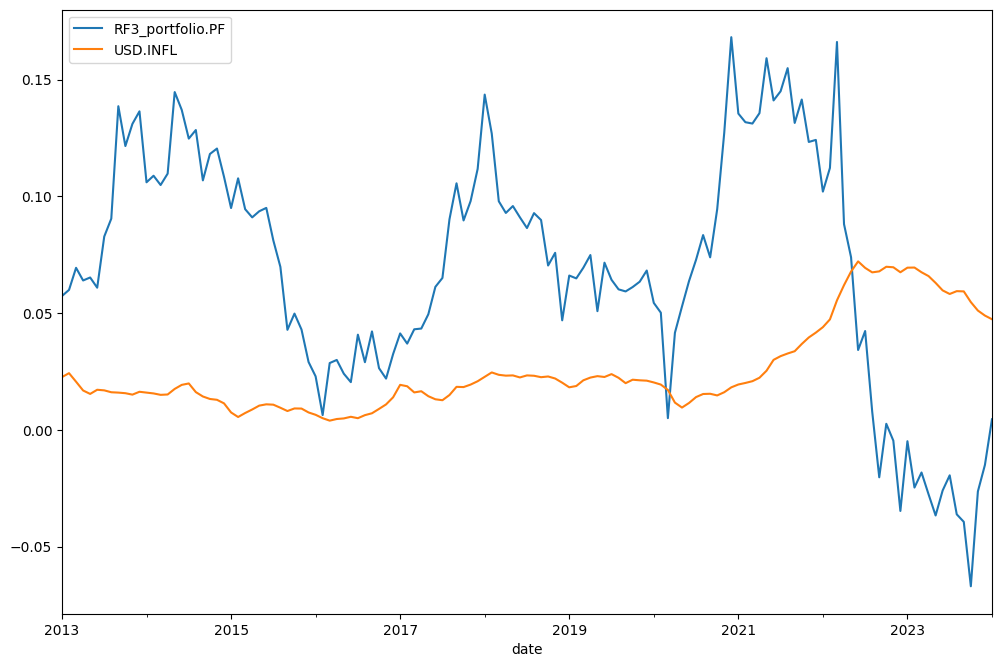

Rolling CAGR for the portfolio is available with get_rolling_cagr:

[29]:

rf3.get_rolling_cagr(

window=12 * 2

).plot(); # window size is in months. We have rolling 2 year CAGR here and rolling 2 year mean inflation ...

The expanding cumulative return time series over a given trailing period can be calculated with get_cumulative_return. The period argument can be expressed in years or as YTD (Year to Date). The last row of the returned DataFrame is the cumulative return over the full selected period.

[ ]:

rf3.get_cumulative_return(

period="YTD"

).tail() # Cumulative return time series since the start of the current calendar year

[ ]:

rf3.get_cumulative_return(period=5).plot(); # Expanding cumulative return time series over the 5 years period

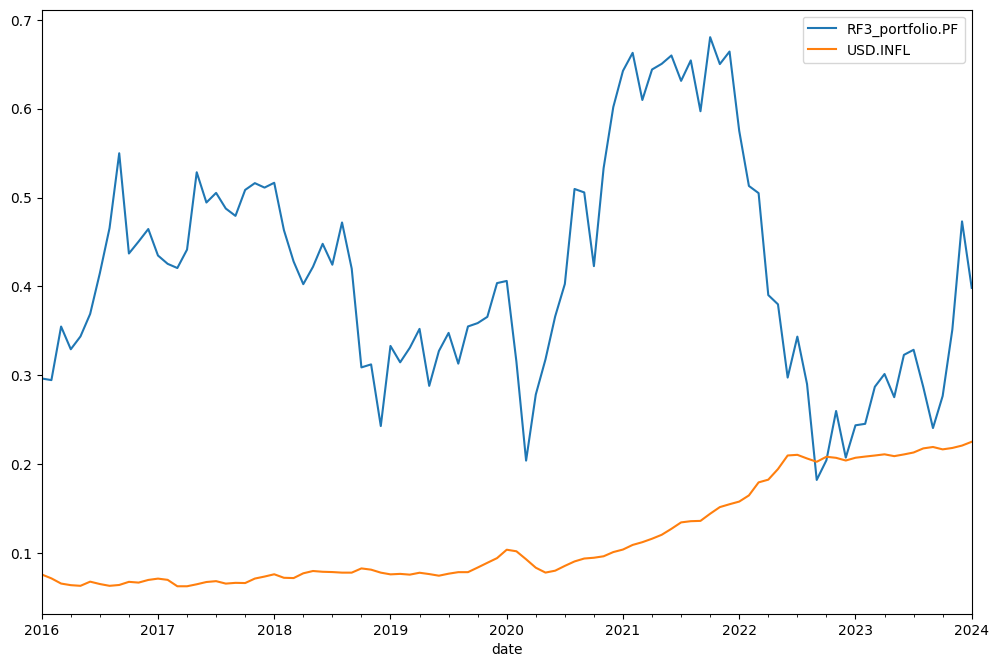

Rolling cumulative return can be helpful in the same situations as rolling CAGR:

[32]:

rf3.get_rolling_cumulative_return(window=12 * 5).plot(); # window size is in months (5 year cumulative return here)

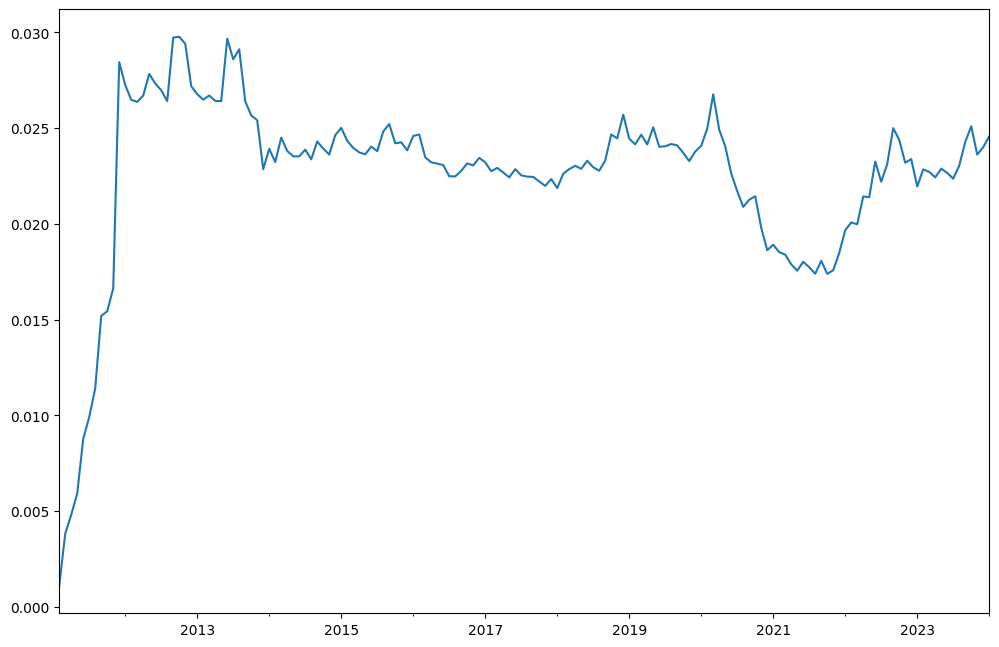

Last-twelve-month (LTM) dividend yield is available through the dividend_yield property.

[33]:

rf3.dividend_yield.plot();

The portfolio also has a monthly dividends time series:

[34]:

rf3.dividends.tail()

[34]:

2025-05 3.416226

2025-06 11.002825

2025-07 3.423926

2025-08 3.529997

2025-09 9.977436

Freq: M, Name: RF3_portfolio.PF, dtype: float64

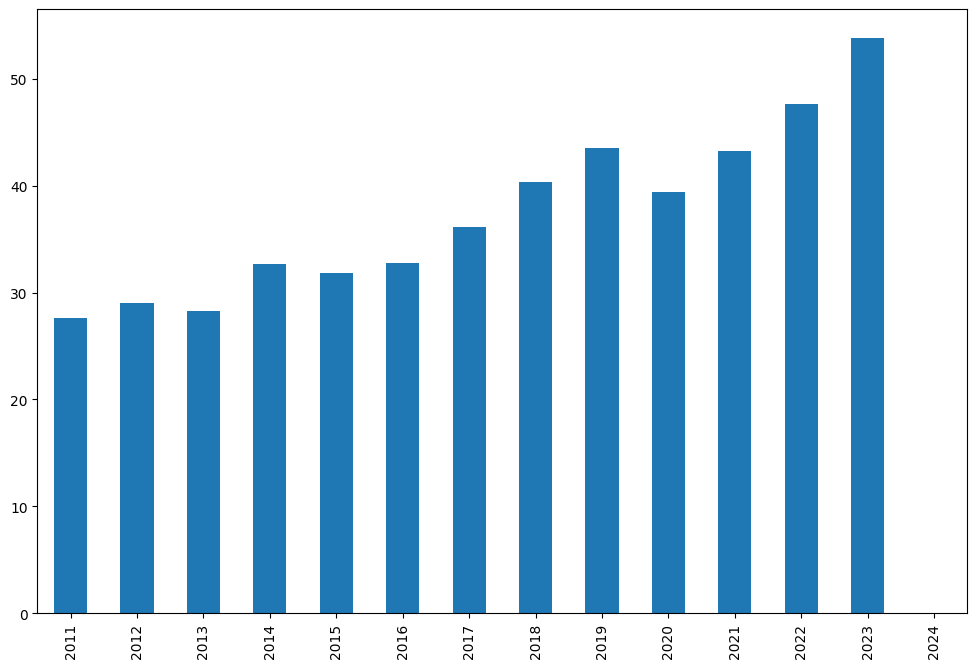

Calendar-year dividend totals are available for the portfolio:

[35]:

rf3.dividends.resample("Y").sum().plot(kind="bar");

Sharpe Ratio was developed by Nobel laureate William F. Sharpe and is used to understand the return of an investment compared to its risk.

\[S_p = \frac{R_p - R_f}{\sigma_p}\]\(R_p\) - expected return of portfolio

[36]:

rf3.get_sharpe_ratio(rf_return=0.02) # risk-free rate is 2% here

[36]:

np.float64(0.5782476698777302)

Finally, the easiest way to inspect the basic properties of a portfolio is with describe:

[37]:

rf3.describe()

[37]:

| property | period | RF3_portfolio.PF | inflation | |

|---|---|---|---|---|

| 0 | compound return | YTD | 0.134785 | 0.028957 |

| 1 | CAGR | 1 years | 0.117922 | 0.030089 |

| 2 | CAGR | 5 years | 0.082588 | 0.045298 |

| 3 | CAGR | 10 years | 0.083948 | 0.031624 |

| 4 | CAGR | 14 years, 8 months | 0.076007 | 0.026678 |

| 5 | Annualized mean return | 14 years, 8 months | 0.077781 | NaN |

| 6 | Dividend yield | LTM | 0.02497 | NaN |

| 7 | Risk | 14 years, 8 months | 0.099924 | NaN |

| 8 | CVAR (α=1) | 14 years, 8 months | 0.177933 | NaN |

| 9 | Max drawdown | 14 years, 8 months | -0.210563 | NaN |

| 10 | Max drawdown date | 14 years, 8 months | 2022-09 | NaN |

Compare several portfolios

A portfolio is a kind of financial asset and can be included in AssetList to compare it with other portfolios, assets, or benchmarks.

Let’s create Rick Ferri’s four-asset portfolio and compare its behavior with the three-asset portfolio.

[38]:

assets = ["BND.US", "VTI.US", "VXUS.US", "VNQ.US"] # Vanguard REIT ETF (VNQ) is added.

weights = [0.40, 0.30, 0.24, 0.06]

To compare it properly with RF3, we should choose the same rebalancing period:

[39]:

rf4 = ok.Portfolio(

assets=assets, weights=weights, rebalancing_strategy=ok.Rebalance(period="year"), symbol="RF4_portfolio.PF"

) # we also give a custom name to portfolio with 'symbol' propety

rf4

[39]:

symbol RF4_portfolio.PF

assets [BND.US, VTI.US, VXUS.US, VNQ.US]

weights [0.4, 0.3, 0.24, 0.06]

rebalancing_period year

rebalancing_abs_deviation None

rebalancing_rel_deviation None

currency USD

inflation USD.INFL

first_date 2011-02

last_date 2025-09

period_length 14 years, 8 months

dtype: object

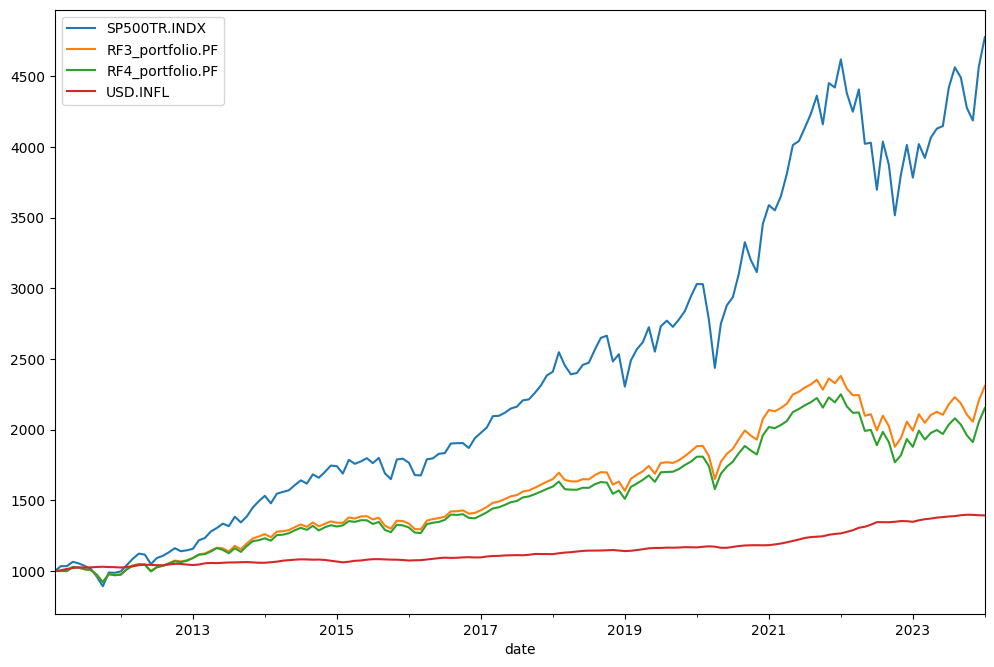

Now we create an AssetList to compare RF3 with RF4 and add a benchmark (the S&P 500 Total Return index).

[40]:

ls = ok.AssetList(["SP500TR.INDX", rf3, rf4])

ls

[40]:

assets [SP500TR.INDX, RF3_portfolio.PF, RF4_portfolio...

currency USD

first_date 2011-03

last_date 2025-09

period_length 14 years, 7 months

inflation USD.INFL

dtype: object

Their behavior can be compared with wealth_indexes:

[41]:

ls.wealth_indexes.plot();

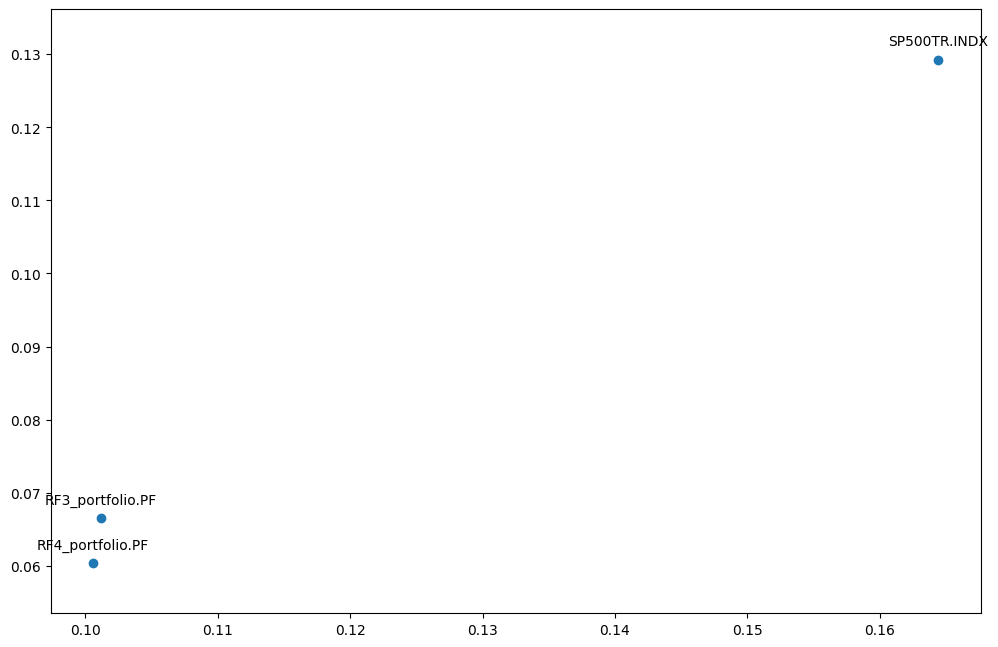

plot_assets. X-axis: Risk (standard deviation)[42]:

ls.plot_assets(kind="cagr"); # set Y-axis to CAGR by kind='cagr'

See06 efficient frontier single period.ipynband07 efficient frontier multi-period.ipynbto plot portfolios together with the Efficient Frontier.

Given a risk-free rate, it is easy to compare the Sharpe ratios of the portfolios with get_sharpe_ratio:

[43]:

ls.get_sharpe_ratio(rf_return=0.02) # Risk-Free rate is 2% here

[43]:

Symbols

SP500TR.INDX 0.742301

RF3_portfolio.PF 0.578248

RF4_portfolio.PF 0.521450

dtype: float64

describe method.YTD (Year to Date) compound return

CAGR for a given list of periods and for the full available history

annualized mean return (arithmetic mean)

LTM dividend yield (last-twelve-month dividend yield)

Risk metrics for the full period:

risk (standard deviation)

CVaR (time frame is 1 year)

maximum drawdowns (and their dates)

[44]:

ls.describe([1, 5, 8]) # portfolio CAGR is shown for YTD, 1, 5, 8 years and for the full histrical period.

[44]:

| property | period | SP500TR.INDX | RF3_portfolio.PF | RF4_portfolio.PF | inflation | |

|---|---|---|---|---|---|---|

| 0 | Compound return | YTD | 0.148334 | 0.134785 | 0.134547 | 0.028957 |

| 1 | CAGR | 1 years | 0.176007 | 0.117922 | 0.105607 | 0.030089 |

| 2 | CAGR | 5 years | 0.164748 | 0.082588 | 0.075639 | 0.045298 |

| 3 | CAGR | 8 years | 0.148874 | 0.078605 | 0.070729 | 0.034951 |

| 4 | CAGR | 14 years, 7 months | 0.138509 | 0.076007 | 0.069573 | 0.026678 |

| 5 | Annualized mean return | 14 years, 7 months | 0.140482 | 0.077781 | 0.071738 | NaN |

| 6 | Dividend yield | LTM | 0.0 | 0.024124 | 0.026396 | NaN |

| 7 | Risk | 14 years, 7 months | 0.162309 | 0.099924 | 0.09922 | NaN |

| 8 | CVAR | 14 years, 7 months | 0.167821 | 0.177933 | 0.181796 | NaN |

| 9 | Max drawdowns | 14 years, 7 months | -0.238631 | -0.210563 | -0.213989 | NaN |

| 10 | Max drawdowns dates | 14 years, 7 months | 2022-09 | 2022-09 | 2022-09 | NaN |

| 11 | Inception date | None | 1988-02 | 2011-02 | 2011-02 | 2011-03 |

| 12 | Last asset date | None | 2025-11 | 2025-09 | 2025-09 | 2025-09 |

| 13 | Common last data date | None | 2025-09 | 2025-09 | 2025-09 | 2025-09 |