okama.Portfolio.plot_hist_fit

- Portfolio.plot_hist_fit(distr='norm', bins=None)

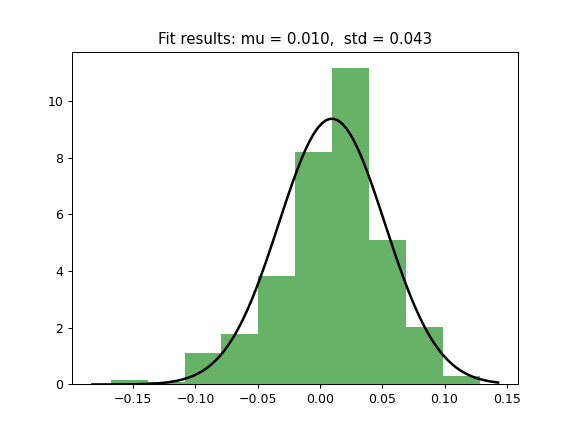

Plot historical distribution histogram for ptrtfolio monthly rate of return time series and theoretical PDF (Probability Distribution Function).

Examples

>>> import matplotlib.pyplot as plt >>> pf = ok.Portfolio(['SP500TR.INDX']) >>> pf.plot_hist_fit(distr='norm') >>> plt.show()