okama.Portfolio.kurtosis_rolling

- Portfolio.kurtosis_rolling(window=60)

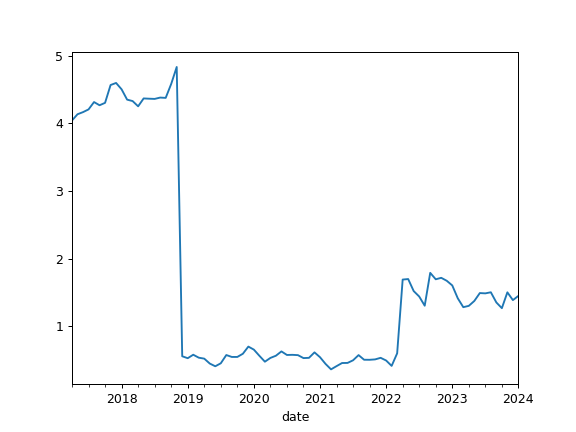

Calculate rolling Fisher (normalized) kurtosis time series for portfolio rate of return.

Kurtosis is a measure of whether the rate of return are heavy-tailed or light-tailed relative to a normal distribution. It should be close to zero for normally distributed rate of return. Kurtosis is the fourth central moment divided by the square of the variance.

- Parameters:

- windowint, default 60

Size of the moving window in months. The window size should be at least 12 months.

- Returns:

- Series

Expanding kurtosis time series.

Examples

>>> pf = ok.Portfolio(['BND.US']) >>> pf.kurtosis_rolling(window=12*10) Date 2017-04 4.041599 2017-05 4.133518 2017-06 4.165099 2017-07 4.205125 2017-08 4.313773 ... 2021-03 0.362184 2021-04 0.409680 2021-05 0.455760 2021-06 0.457315 2021-07 0.496168 Freq: M, Name: portfolio_4411.PF, dtype: float64

>>> import matplotlib.pyplot as plt >>> pf.kurtosis_rolling(window=12*10).plot() >>> plt.show()