plot_pair_ef

- EfficientFrontier.plot_pair_ef(tickers='tickers', figsize=None)

Plot Efficient Frontier for every pair of assets.

Efficient Frontier is a set of portfolios which satisfy the condition that no other portfolio exists with a higher expected return but with the same risk (standard deviation of return).

- Parameters:

- tickers{‘tickers’, ‘names’, ‘local_names’} or list[str], default ‘tickers’

Annotation type for assets. ‘tickers’ - assets symbols are shown in form of ‘SPY.US’ ‘names’ - assets names are used like - ‘SPDR S&P 500 ETF Trust’ ‘local_names’ - native-language names (e.g. ‘Сбербанк’ / ‘贵州茅台’) To show custom annotations for each asset pass the list of names.

- figsizetuple[float, float], default None

Figure size (width, height) in inches. If None, matplotlib default is used.

- Returns:

- Axes

Matplotlib axes with the plot.

Notes

At least 3 assets are required.

Examples

>>> import matplotlib.pyplot as plt

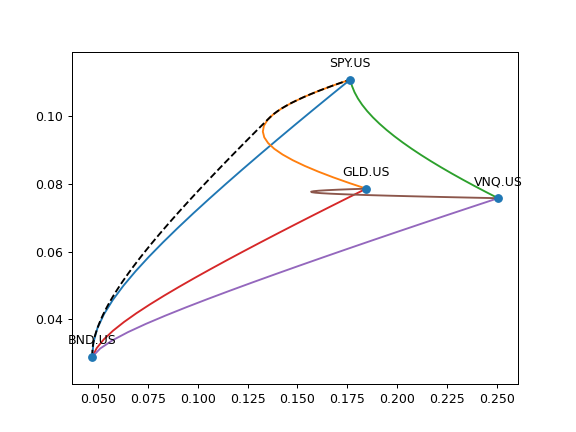

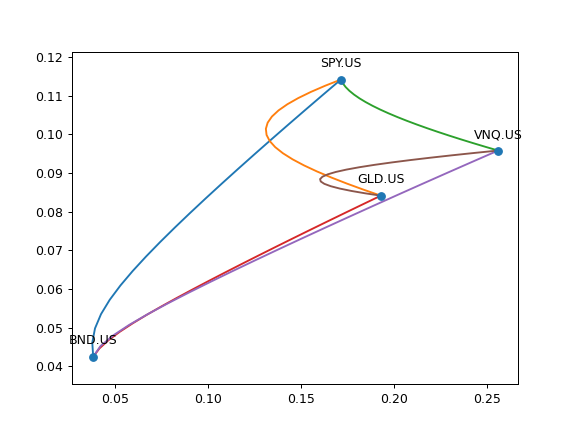

>>> ls4 = ["SPY.US", "BND.US", "GLD.US", "VNQ.US"] >>> curr = "USD" >>> last_date = "2021-07" >>> ef = ok.EfficientFrontier(ls4, ccy=curr, last_date=last_date) >>> ef.plot_pair_ef() >>> plt.show()

It can be useful to plot the full Efficient Frontier (EF) with optimized 4 asset portfolios together with the EFs for each pair of assets.

>>> ef4 = ok.EfficientFrontier(assets=ls4, ccy=curr, n_points=100) >>> df4 = ef4.ef_points >>> fig = plt.figure() >>> # Plot Efficient Frontier for every pair of assets. Optimized portfolios will have 2 assets. >>> ef4.plot_pair_ef() # CAGR is used for optimized portfolios. >>> ax = plt.gca() >>> # Plot the full Efficient Frontier for 4 asset portfolios. >>> ax.plot(df4["Risk"], df4["CAGR"], color="black", linestyle="--") >>> plt.show()