get_monte_carlo

- EfficientFrontier.get_monte_carlo(n=100)

Generate random rebalanced portfolios with Monte Carlo simulation.

Risk (annualized standard deviation) and return (CAGR) are calculated for random weights within bounds.

- Parameters:

- nint, default 100

Number of random portfolios to generate with Monte Carlo simulation.

- Returns:

- DataFrame

Table with Return (CAGR) and Risk values for random portfolios (portfolios with random asset weights).

Examples

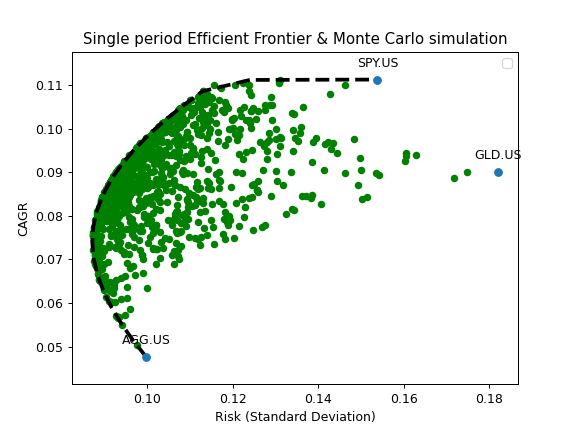

>>> ls_m = ["SPY.US", "GLD.US", "PGJ.US", "RGBITR.INDX", "MCFTR.INDX"] >>> curr_rub = "RUB" >>> x = ok.EfficientFrontier( ... assets=ls_m, ... first_date="2005-01", ... last_date="2020-11", ... ccy=curr_rub, ... rebalancing_strategy=ok.Rebalance(period="year"), # set rebalancing period to one year ... n_points=20, ... verbose=False, ... ) >>> monte_carlo = x.get_monte_carlo(n=1000) # it can take some time ... >>> monte_carlo.head(5) CAGR Risk 0 0.182937 0.178518 1 0.184915 0.172965 2 0.154892 0.141681 3 0.185500 0.168739 4 0.176748 0.192657

Monte Carlo simulation results can be plotted together with the optimized portfolios on the Efficient Frontier.

>>> import matplotlib.pyplot as plt

>>> df_reb_year = x.ef_points # optimize portfolios for EF. Calculations will take some time ... >>> fig = plt.figure() >>> # Plot the assets points (optional). >>> x.plot_assets(kind="cagr") >>> ax = plt.gca() >>> # Plot random portfolios (Monte Carlo simulation) >>> ax.scatter(monte_carlo.Risk, monte_carlo.CAGR) >>> # Plot the Efficient Frontier >>> ax.plot(df_reb_year.Risk, df_reb_year.CAGR, label="Annually rebalanced") >>> # Set the axis labels and Title >>> ax.set_title("Multi-period Efficient Frontier & Monte Carlo simulation") >>> ax.set_xlabel("Risk (Standard Deviation)") >>> ax.set_ylabel("CAGR") >>> ax.legend() >>> plt.show()