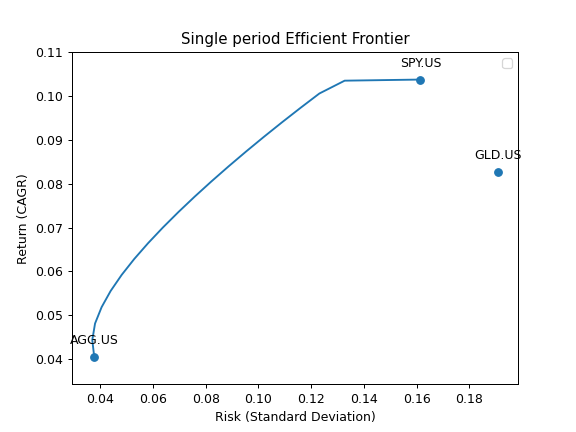

ef_points

- property EfficientFrontier.ef_points

Generate multi-period Efficient Frontier.

Each point on the Efficient Frontier is a rebalanced portfolio with optimized annual risk for a given CAGR. In case of non-convexity along the risk axis, the second part of the chart is generated, where the maximum risk value is found for each point.

- Returns:

- DataFrame

Table of weights and risk/return values for the Efficient Frontier. The columns:

assets weights

CAGR

Risk (standard deviation)

All the values are annualized.

Examples

>>> ls = ["SPY.US", "GLD.US"] >>> curr = "USD" >>> y = ok.EfficientFrontier( ... assets=ls, ... first_date="2004-12", ... last_date="2020-10", ... ccy=curr, ... rebalancing_strategy=ok.Rebalance(period="year"), ... ticker_names=True, # Use tickers in DataFrame column names. ... n_points=20, # Number of points in the Efficient Frontier. ... ) >>> df_reb_year = y.ef_points >>> df_reb_year[["Risk", "CAGR", "SPY.US", "GLD.US"]].head(5) Risk CAGR SPY.US GLD.US 0 0.159403 0.087770 1.000000 0.000000 1 0.157208 0.088178 0.985742 0.014258 2 0.155011 0.088586 0.971065 0.028935 3 0.152814 0.088994 0.955931 0.044069 4 0.150619 0.089402 0.940300 0.059700

To compare the Efficient Frontiers of annually rebalanced portfolios with not rebalanced portfolios it’s possible to draw 2 charts: rebalancing_strategy=ok.Rebalance(period=’year’) and ok.Rebalance(period=’none’).

>>> import matplotlib.pyplot as plt

>>> y.rebalancing_strategy = ok.Rebalance(period="none") >>> df_not_reb = y.ef_points >>> fig = plt.figure() >>> # Plot the assets points using CAGR to match the Efficient Frontier Y-axis. >>> ax = y.plot_assets(kind="cagr") >>> # Plot the Efficient Frontier for annually rebalanced portfolios >>> ax.plot(df_reb_year["Risk"], df_reb_year["CAGR"], label="Annually rebalanced") >>> # Plot the Efficient Frontier for not rebalanced portfolios >>> ax.plot(df_not_reb["Risk"], df_not_reb["CAGR"], label="Not rebalanced") >>> # Set axis labels and the title >>> ax.set_title("Multi-period Efficient Frontier: 2 assets") >>> ax.set_xlabel("Risk (Standard Deviation)") >>> ax.set_ylabel("Return (CAGR)") >>> ax.legend() >>> plt.show()