wealth_index

- PortfolioDCF.wealth_index(discounting, include_negative_values=False)

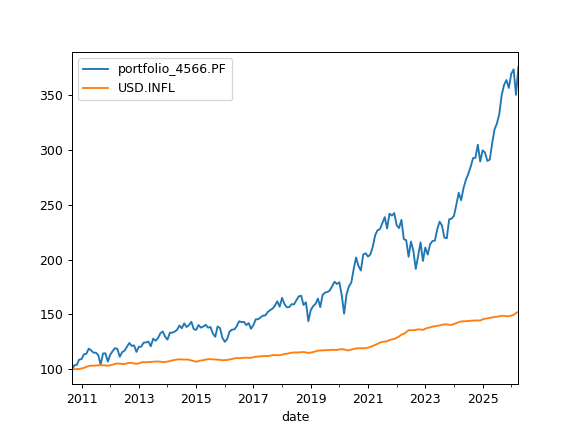

Calculate wealth index time series for the portfolio with cash flow (contributions and withdrawals) using historical rate of returns.

Wealth index (Cumulative Wealth Index) is a time series that presents the value of portfolio over historical time period considering cash flows.

Accumulated inflation time series is added if inflation=True in the Portfolio.

If there is no cash flow, Wealth index is obtained from the accumulated return multiplied by the initial investments. That is: initial_investment * (Accumulated_Return + 1)

- Parameters:

- discounting{‘fv’, ‘pv’}

Type of discounting to apply: - ‘fv’: Future Values - nominal values without discounting - ‘pv’: Present Values - values discounted to present using the discount rate

- include_negative_valuesbool, default False

Whether to include negative wealth index values in the result. If False, negative values are replaced with zeros.

- Returns:

- pd.DataFrame

Time series of wealth index values for portfolio and accumulated inflation (if applicable).

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio(["VOO.US", "GLD.US"], weights=[0.8, 0.2]) >>> ind = ok.IndexationStrategy(pf) # Set Cash Flow Strategy parameters >>> ind.initial_investment = 100 # initial investments value >>> ind.frequency = "year" # withdrawals frequency >>> ind.amount = -6 # initial withdrawals amount >>> ind.indexation = "inflation" # the indexation is equal to inflation >>> pf.dcf.cashflow_parameters = ind # assign the strategy to Portfolio >>> pf.dcf.wealth_index(discounting="fv", include_negative_values=False).plot() >>> plt.show()