monte_carlo_cash_flow

- PortfolioDCF.monte_carlo_cash_flow(discounting, remove_if_wealth_index_negative=True)

Calculate portfolio random cash flow (withdrawals/contributions) time series by Monte Carlo simulation.

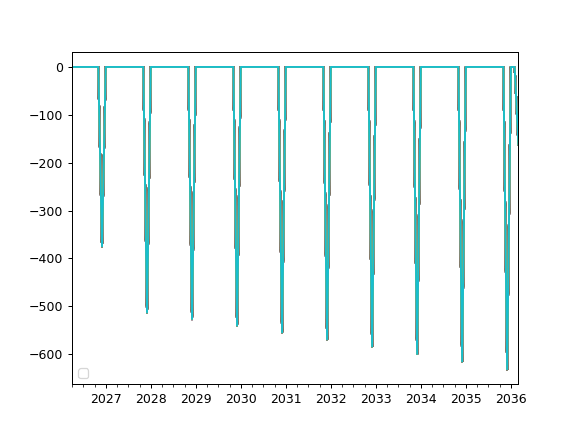

Monte Carlo simulation generates n random monthly time series of cash flows. Each cash flow time series corresponds to a wealth index calculated with rate of return time series of a given distribution.

First date of forecasted returns is portfolio last_date.

- Parameters:

- discounting{‘fv’, ‘pv’}

Type of discounting to apply: - ‘fv’: Future Values - nominal values without discounting - ‘pv’: Present Values - values discounted to present using the discount rate

- remove_if_wealth_index_negativebool, default True

If True, cash flow values are replaced with 0 when wealth index is negative (or zero).

- Returns:

- DataFrame

Table with n random cash flow monthly time series.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio( ... ["SPY.US", "AGG.US", "GLD.US"], ... weights=[0.60, 0.35, 0.05], ... rebalancing_strategy=ok.Rebalance(period="month"), ... ) >>> pf.dcf.set_mc_parameters(distribution="t", period=10, mc_number=100) # Set Monte Carlo parameters >>> # set cash flow parameters >>> ind = ok.IndexationStrategy(pf) # create cash flow strategy linked to the portfolio >>> ind.initial_investment = 10_000 # add initial investment to cash flow strategy >>> ind.amount = -500 # set withdrawal size >>> ind.frequency = "year" # set withdrawal frequency >>> pf.dcf.cashflow_parameters = ind # assign cash flow strategy to portfolio >>> pf.dcf.monte_carlo_cash_flow(discounting="fv").plot() >>> plt.legend("") # don't show legend for each line >>> plt.show()