mdp_points

- property EfficientFrontier.mdp_points

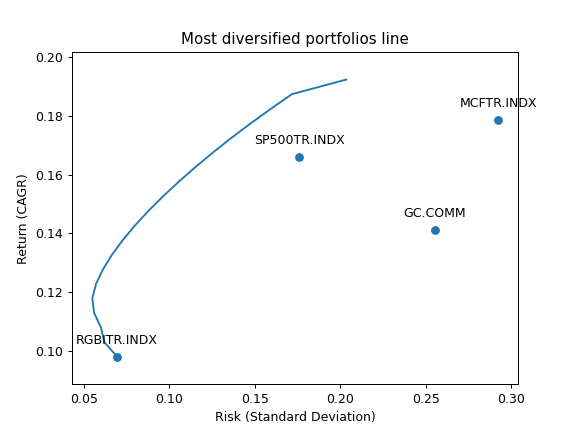

Generate Most diversified portfolios frontier for rebalanced portfolios.

Each point on the Most diversified portfolios frontier is a rebalanced portfolio with optimized Diversification ratio for a given CAGR.

The points are obtained through the constrained optimization process (optimization with bounds). Bounds are defined with ‘bounds’ property.

- Returns:

- DataFrame

Table of weights and risk/return values for the Most Diversified Portfolios Frontier. The columns:

assets weights

CAGR (geometric mean)

Risk (standard deviation)

Diversification ratio

All the values are annualized.

Examples

>>> ls4 = ["SP500TR.INDX", "MCFTR.INDX", "RGBITR.INDX", "GC.COMM"] >>> y = ok.EfficientFrontier(assets=ls4, ccy="RUB", last_date="2021-12", n_points=20) >>> y.mdp_points # print mdp weights, risk, CAGR and Diversification ratio Risk CAGR Diversification ratio ... MCFTR.INDX RGBITR.INDX SP500TR.INDX 0 0.066040 0.092220 1.234567 ... 2.081668e-16 1.000000e+00 0.000000e+00 1 0.064299 0.093451 1.245678 ... 0.000000e+00 9.844942e-01 5.828671e-16 ...

To plot the Most diversification portfolios line use the DataFrame with the points data. Additionally ‘Plot.plot_assets()’ can be used to show the assets in the chart.

>>> import matplotlib.pyplot as plt

>>> fig = plt.figure() >>> # Plot the assets points >>> y.plot_assets(kind="cagr") # kind should be set to "cagr" as we take "CAGR" column from the mdp_points. >>> ax = plt.gca() >>> # Plot the Most diversified portfolios line >>> df = y.mdp_points >>> ax.plot(df["Risk"], df["CAGR"]) # we chose to plot CAGR which is geometric mean of return series >>> # Set the axis labels and the title >>> ax.set_title("Most diversified portfolios line") >>> ax.set_xlabel("Risk (Standard Deviation)") >>> ax.set_ylabel("Return (CAGR)") >>> plt.show()