plot_forecast_monte_carlo

- PortfolioDCF.plot_forecast_monte_carlo(backtest=True, figsize=None)

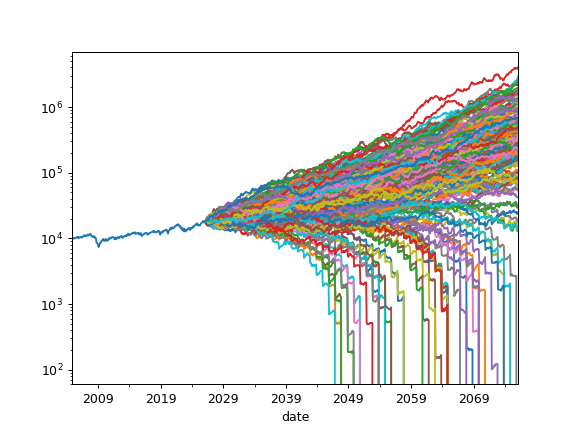

Plot Monte Carlo simulation for portfolio future wealth indexes optionally together with historical wealth index.

Wealth index (Cumulative Wealth Index) is a time series that presents the value of portfolio over time period considering cash flows (portfolio withdrawals/contributions).

Random wealth indexes are generated according to a given distribution.

- Parameters:

- backtestbool, default True

Include historical wealth index if True.

- figsizetuple of (float, float), default None

Figure size (width, height) in inches. If None, matplotlib defaults are used.

- Returns:

- Axes

Matplotlib axes object.

Examples

>>> import matplotlib.pyplot as plt

>>> pf = ok.Portfolio( ... assets=["SPY.US", "AGG.US", "GLD.US"], ... weights=[0.60, 0.35, 0.05], ... rebalancing_strategy=ok.Rebalance(period="year"), ... ) >>> # Set Monte Carlo parameters >>> pf.dcf.set_mc_parameters(distribution="norm", period=50, mc_number=200) >>> # set cash flow parameters >>> ind = ok.IndexationStrategy(pf) # create cash flow strategy linked to the portfolio >>> ind.initial_investment = 10_000 # add initial investment to cash flow strategy >>> ind.amount = -500 # set withdrawal size >>> ind.frequency = "year" # set withdrawal frequency >>> pf.dcf.cashflow_parameters = ind # assign cash flow strategy to portfolio >>> pf.dcf.plot_forecast_monte_carlo(backtest=True) >>> plt.yscale("log") # Y-axis has logarithmic scale >>> plt.show()